We have a global intelligence crisis, in that a lot of people are being really fucking stupid.

As I discussed in this week’s free piece, alleged financial analyst Citrini Research put out a truly awful screed called the “2028 Global Intelligence Crisis” — a slop-filled scare-fiction written and framed with the authority of deeply-founded analysis, so much so that it caused a global selloff in stocks.

At 7,000 words, you’d expect the piece to have some sort of argument or base in reality, but what it actually says is that “AI will get so cheap that it will replace everything, and then most white collar people won’t have jobs, and then they won’t be able to pay their mortgages, also AI will cause private equity to collapse because AI will write all software.”

This piece is written specifically to spook *and* ingratiate anyone involved in the financial markets with the idea that their investments are bad but investing in AI companies is good, and also that if they don't get behind whatever this piece is about (which is unclear!), they'll be subject to a horrifying future where the government creates a subsidy generated by a tax on AI inference (seriously). And, most damningly, its most important points about HOW this all happens are single sentences that read "and then AI becomes more powerful and cheaper too and runs on a device."

Part of the argument is that AI agents will use cryptocurrency to replace MasterCard and Visa. It’s dogshit. I’m shocked that anybody took it seriously.

The fact this moved markets should suggest that we have a fundamentally flawed financial system — and here’s an annotated version with my own comments.

This is the second time our markets have been thrown into the shitter based on AI booster hype. A mere week and a half ago, a software sell-off began because of the completely fanciful and imaginary idea that AI would now write all software.

I really want to be explicit here: AI does not threaten the majority of SaaS businesses, and they are jumping at ghost stories.

If I am correct, those dumping software stocks believe that AI will replace these businesses because people will be able to code their own software solutions. This is an intellectually bankrupt position, one that shows an alarming (and common) misunderstanding of very basic concepts. It is not just a matter of “enough prompts until it does this” — good (or even functional!) software engineering is technical, infrastructural, and philosophical, and the thing you are “automating” is not just the code that makes a thing run.

Let's start with the simplest, and least-technical way of putting it: even in the best-case scenario, you do not just type "Build Be A Salesforce Competitor" and it erupts, fully-formed, from your Terminal window. It is not capable of building it, but even if it were, it would need to actually be on a cloud hosting platform, and have all manner of actual customer data entered into it. Building software is not writing code and then hitting enter and a website appears, requiring all manner of infrastructural things (such as "how does a customer access it in a consistent and reliable way," "how do I make sure that this can handle a lot of people at once," and "is it quick to access," with the more-complex database systems requiring entirely separate subscriptions just to keep them connecting).

Software is a tremendous pain in the ass. You write code, then you have to make sure the code actually runs, and that code needs to run in some cases on specific hardware, and that hardware needs to be set up right, and some things are written in different languages, and those languages sometimes use more memory or less memory and if you give them the wrong amounts or forget to close the door in your code on something everything breaks, sometimes costing you money or introducing security vulnerabilities.

In any case, even for experienced, well-versed software engineers, maintaining software that involves any kind of customer data requires significant investments in compliance, including things like SOC-2 audits if the customer itself ever has to interact with the system, as well as massive investments in security.

And yet, the myth that LLMs are an existential threat to existing software companies has taken root in the market, sending the share prices of the legacy incumbents tumbling. A great example would be SAP, down 10% in the last month.

SAP makes ERP (Enterprise Resource Planning, which I wrote about in the Hater's Guide To Oracle) software, and has been affected by the sell-off. SAP is also a massive, complex, resource-intensive database-driven system that involves things like accounting, provisioning and HR, and is so heinously complex that you often have to pay SAP just to make it function (if you're lucky it might even do so). If you were to build this kind of system yourself, even with "the magic of Claude Code" (which I will get to shortly), it would be an incredible technological, infrastructural and legal undertaking.

Most software is like this. I’d say all software that people rely on is like this. I am begging with you, pleading with you to think about how much you trust the software that’s on every single thing you use, and what you do when a piece of software stops working, and how you feel about the company that does that. If your money or personal information touches it, they’ve had to go through all sorts of shit that doesn’t involve the code to bring you the software.

Sidenote: I want to be clear that there is nothing good about this. To quote a friend of mine — an editor at a large tech publication — “Oracle is a lawfirm with a software company attached.” SaaS companies regularly get by through scurrilous legal means and bullshit contracts, and their features are, in many cases, only as good as they need to be. Regardless, my point is that you will not just “make your own software.”

Any company of a reasonable size would likely be committing hundreds of thousands if not millions of dollars of legal and accounting fees to make sure it worked, engineers would have to be hired to maintain it, and you, as the sole customer of this massive ERP system, would have to build every single new feature and integration you want. Then you'd have to keep it running, this massive thing that involves, in many cases, tons of personally identifiable information. You'd also need to make sure, without fail, that this system that involves money was aware of any and all currencies and how they fluctuate, because that is now your problem. Mess up that part and your system of record could massively over or underestimate your revenue or inventory, which could destroy your business.

If that happens, you won't have anyone to sue. When bugs happen, you'll have someone who's job it is to fix it that you can fire, but replacing them will mean finding a new person to fix the mess that another guy made.

And then we get to the fact that building stuff with Claude Code is not that straightforward. Every example you've read about somebody being amazed by it has built a toy app or website that's very similar to many open source projects or website templates that Anthropic trained its training data on.

Every single piece of SaaS anyone pays for is paying for both access to the product and a transfer of the inherent risk or chaos of running software that involves people or money. Claude Code does not actually build unique software. You can say "create me a CRM," but whatever CRM it pops out will not magically jump onto Amazon Web Services, nor will it magically be efficient, or functional, or compliant, or secure, nor will it be differentiated at all from, I assume, the open source or publicly-available SaaS it was trained on. You really still need engineers, if not more of them than you had before.

It might tell you it's completely compliant and that it will run like a hot knife through butter — but LLMs don’t know anything, and you cannot be sure Claude is telling the truth as a result. Is your argument that you’d still have a team of engineers (so they know what the outputs mean), but they’d be working on replacing your SaaS subscription? You’re basically becoming a startup with none of the benefits.

To quote Nik Suresh, an incredibly well-credentialed and respected software engineer (author of I Will Fucking Piledrive You If You Mention AI Again), “...for some engineers, [Claude Code] is a great way to solve certain, tedious problems more quickly, and the responsible ones understand you have to read most of the output, which takes an appreciable fraction of the time it would take to write the code in many cases. Claude doesn't write terrible code all the time, it's actually good for many cases because many cases are boring. You just have to read all of it if you aren't a fucking moron because it periodically makes company-ending decisions.”

Just so you know, “company-ending decisions” could start with your vibe-coded Stripe clone leaking user credit card numbers or social security numbers because you asked it to “just handle all the compliance stuff.” Even if you have very talented engineers, are those engineers talented in the specifics of, say, healthcare data or finance? They’re going to need to be to make sure Claude doesn’t do anything stupid!

The Intelligence Crisis In Private Investing and Private Equity

So, despite all of this being very obvious, it’s clear that the markets and an alarming number of people in the media simply do not know what they are talking about. The “AI replaces software” story is literally “Anthropic has released a product and now the resulting industry is selling off,” such as when it launched a cybersecurity tool that could check for vulnerabilities (a product that has existed in some form for nearly a decade) causing a sell-off in cybersecurity stocks like Crowdstrike — you know, the one that had a faulty bit of code cause a global cybersecurity incident that lost the Fortune 500 billions, and led to Delta Air Lines suspending over 1,200 flights over six long days of disruption.

There is no rational basis for anything about this sell-off other than that our financial media and markets do not appear to understand the very basic things about the stuff they invest in. Software may seem complex, but (especially in these cases) it’s really quite simple: investors are conflating “an AI model can spit out code” with “an AI model can create the entire experience of what we know as “software,” or is close enough that we have to start freaking out.”

This is thanks to the intentionally-deceptive marketing pedalled by Anthropic and validated by the media. In a piece from September 2025, Bloomberg reported that Claude Sonnet 4.5 could “code on its own for up to 30 hours straight,” a statement directly from Anthropic repeated by other outlets that added that it did so “on complex, multi-step tasks,” none of which were explained. The Verge, however, added that apparently Anthropic “coded a chat app akin to Slack or Teams,” and no, you can’t see it, or know anything about how much it costs or its functionality. Does it run? Is it useful? Does it work in any way? What does it look like? We have absolutely no proof this happened other than them saying it, but because the media repeated it it’s now a fact.

Perhaps it’s not a particularly novel statement, but it’s becoming kind of obvious that maybe the people with the money don’t actually know what they’re doing, which will eventually become a problem when they all invest in the wrong thing for the wrong reasons.

SaaS (Software as a Service, which almost always refers to business software) stocks became a hot commodity because they were perpetual growth machines with giant sales teams that existed only to make numbers go up, leading to a flurry of investment based on the assumption that all numbers will always increase forever, and every market is as giant as we want. Not profitable? No problem! You just had to show growth.

It was easy to raise money because everybody saw a big, obvious path to liquidity, either from selling to a big firm or taking the company public…

…in theory.

How Private Equity Created A Pump-And-Dump Crisis In Software By Assuming Everything Would Grow Forever — And Everything Broke In 2021

Per Victor Basta, between 2014 and 2017, the number of VC rounds in technology companies halved with a much smaller drop in funding, adding that a big part was the collapse of companies describing themselves as SaaS, which dropped by 40% in the same period. In a 2016 chat with VC David Yuan, Gainsight CEO Nick Mehta added that “the bar got higher and weights shifted in the public markets,” citing that profitability was now becoming more important to investors.

Per Mehta, one savior had arrived — Private Equity, with Thoma Bravo buying Blue Coat Systems in 2011 for $1.3 billion (which had been backed by a Canadian teacher’s pension fund!), Vista Equity buying Tibco for $4.3 billion in 2014, and Permira Advisers (along with the Canadian Pension Plan Investment Board) buying Informatica for $5.3 billion (with participation from both Salesforce and Microsoft) in 2015, 16 years after its first IPO. In each case, these firms were purchased using debt that immediately gets dumped onto the company’s balance sheet, known as a leveraged buyout.

In simple terms, you buy a company with money that the company you just bought has to pay off. The company in question also has to grow like gangbusters to keep up with both that debt and the private equity firm’s expectations. And instead of being an investor with a board seat who can yell at the CEO, it’s quite literally your company, and you can do whatever you want with (or to) it.

Yuan added that the size of these deals made the acquisitions problematic, as did their debt-filled:

Recent SaaS PE deals are different. At more than six times revenues, unless you can increase EBITDA margins to over 40%, it’s hard to get your arms around the effective EBITDA multiple. It seems the new breed of PE buyer is taking a bet that SaaS companies will exit on revenue multiples and show rapid growth over many years. Both are arguably new bets for private equity. It’s not about financial or cost engineering. They are starting to look a bit more like us in the growth investing industry and taking a bet on category leadership and growth

…

So while revenue multiples are accepted, they are viewed as risky by private equity. Take Salesforce.com, the bellwether of SaaS. Over the last 10 years, it’s traded below 2 times next-twelve-months (NTM) revenues and over 10 times NTM revenues. Even in the past 12 months, it’s traded as low as 4.7 times NTM multiples and as high as close to 9 times NTM multiples. In this example, if the private equity firm paid 9 times NTM revenues and multiples traded down to 4.7 times NTM, their $300 million in equity would be wiped out. In fact, they would owe the bank close to $100 million. Now it’s not that bad, as these companies are growing revenue at the same time. But it does show you why private equity has largely been wary of revenue multiples and have relied on EBITDA and free cash flow multiples.

Symantec would acquire Blue Coat for $4.65 billion in 2016, for just under a 4x return. Things were a little worse for Tibco. Vista Equity Partners tried to sell it in 2021 amid a surge of other M&A transactions, with the solution — never change, private equity! — being to buy Citrix for $16.5 billion (a 30%% premium on its stock price) and merge it with Tibco, magically fixing the problem of “what do we do with Tibco?” by hiding it inside another transaction. Informatica eventually had a $10 billion IPO in 2021, which was flat in its first day of trading, never really did more than stay at its IPO price, then sold to Salesforce for $8 billion in 2025, at an equity value of $8 billion, which seems fine but not great until you realize that, with inflation, the $5.3 billion that Permira invested in 2015 was about $7.15 billion in 2025’s money.

In every case, the assumption was very simple: these businesses would grow and own their entire industries, the PE firm would be the reason they did this (by taking them private and filling them full of debt while making egregious growth demands), and the meteoric growth of SaaS would continue in perpetuity.

Yet the real year that broke things was 2021. As everybody returned to the real world, consumer and business spending skyrocketed, leading (per Bloomberg) to a massive surge in revenues that convinced private equity to shove even more cash and debt up the ass of SaaS:

The sector has been a hugely popular target for buyout firms and their private credit cousins. From 2015 to 2025, more than 1,900 software companies were taken over by private equity buyers in transactions valued at more than $440 billion, according to data compiled by Bloomberg.

Deals were easily waved through most investment committees because the model was simple. Revenues are “sticky” because the tech is embedded into businesses, helping with everything from payroll to HR, and the subscription fee model meant predictable cash flows.

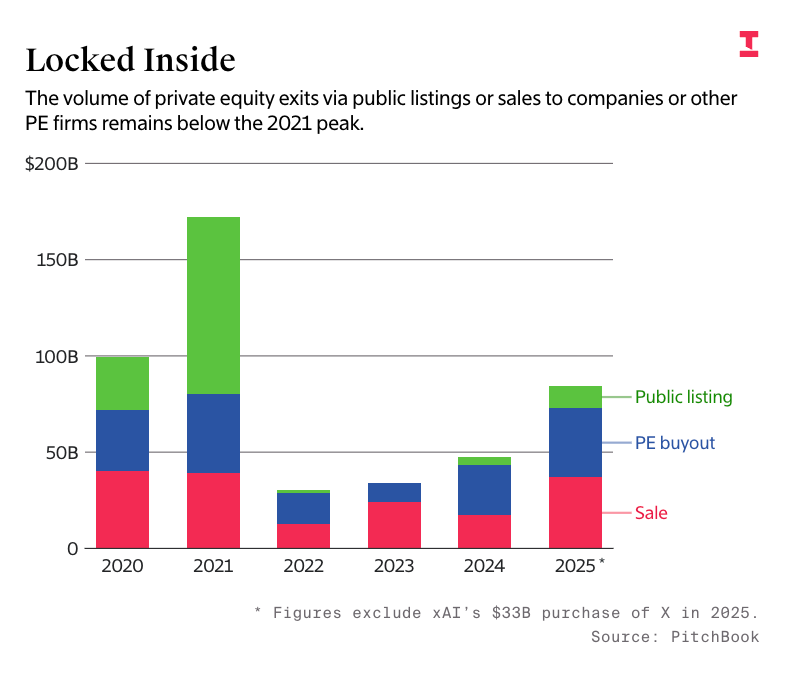

Bloomberg is a little nicer than I am, so they’re not just writing “deals were waved through because everybody assumed that software grows forever and nobody actually knew a thing about the technology or why it would grow so fast.” Unsurprisingly, this didn’t turn out to be true. Per The Information, PE firms invested in or bought 1,167 U.S. software companies for $202 billion, and usually hold investments for three to five years. Thankfully, they also included a chart to show how badly this went:

2021 was the year of overvaluation, and (per Jason Lemkin of SaaStr) 60% of unicorns (startups with $1bn+) valuations hadn’t raised funds in years. The massive accumulated overinvestment, combined with no obvious pathway to an exit, led to people calling these companies “Zombie Unicorns”:

A reckoning that has been looming for years is becoming painfully tangible. In 2021 more than 354 companies received billion-dollar valuations, thus achieving unicorn status. Only six of them have since held IPOs, says Ilya Strebulaev, a professor at Stanford Graduate School of Business. Four others have gone public through SPACs, and another 10 have been acquired, several for less than $1 billion.

Welcome to the era of the zombie unicorn. There are a record 1,200 venture-backed unicorns that have yet to go public or get acquired, according to CB Insights, a researcher that tracks the venture capital industry. Startups that raised large sums of money are beginning to take desperate measures. Startups in later stages are in a particularly difficult position, because they generally need more money to operate—and the investors who’d write checks at billion-dollar-plus valuations have gotten more selective. For some, accepting unfavorable fundraising terms or selling at a steep discount are the only ways to avoid collapsing completely, leaving behind nothing but a unicorpse.

The problem, to quote The Information, is that “PE firms don’t want to lock in returns that are lower than what they promised their backers, say some executives at these firms,” and “many enterprise software firms’ revenue growth has slowed.”

Easy Money and Easy Exits Caused Venture Capital and Private Equity To Over-Extend Themselves, Optimizing For Growth Rather Than Investing In Companies That Were Actually Valuable

Per CNBC in November 2025, private equity firms were facing the same zombie problem:

These so-called “zombie companies” refer to businesses that aren’t growing, barely generate enough cash to service debt and are unable to attract buyers even at a discount. They are usually trapped on a fund’s balance sheet beyond its expected holding period. “Now, as interest rates were rising, people felt they were stuck with businesses that were slightly worthless, but they couldn’t really sell them … So you are in this awful situation where people throw around the word zombie companies,” Oliver Haarmann, founding partner of private investment firm Searchlight Capital Partners, told CNBC’s ” Squawk Box Europe ” on Tuesday.

Per Jason Lemkin, private equity is sitting on its largest collection of companies held for longer than four years since 2012, with McKinsey estimating that more than 16,000 companies (more than 52% of the total buyout-backed inventory) had been held by private equity for more than four years, the highest on record.

In very simple terms, there are hundreds of billions of tech companies sitting in the wings of private equity firms that they’re desperate to sell, with the only customers being big tech firms, other private equity firms, and public offerings in one of the slowest IPO markets in history.

Investing used to be easy. There were so many ideas for so many companies, companies that could be worth billions of dollars once they’d been fattened up with venture capital and/or private equity. There were tons of acquirers, it was easy to take them public, and all you really had to do was exist and provide capital. Companies didn’t have to be good, they just had to look good enough to sell.

This created a venture capital and private equity industry based on symbolic value, and chased out anyone who thought too hard about whether these companies could actually survive on their own merits.

Per PitchBook, since 2022, 70% of VC-backed exits were valued at less than the capital put in, with more than a third of them being startups buying other startups in 2024. Private equity firms are now holding assets for an average of 7 years,

McKinsey also added one horrible detail for the overall private equity market, emphasis mine:

PE returns have not only trended downward over time; they appear to be at a historic low. Buyout fund IRRs (internal rate of return) reached a post-2002 trough between 2022 and 2025, averaging 5.7 percent on a pooled basis and ranking as the second-lowest period on a median basis at 5.4 percent. This deterioration reflects a combination of paying more (entry valuations are higher), macroeconomic uncertainty (inflation and higher interest rates especially hurt overall returns), and a persistently challenged realization environment (assets are harder to sell).

You see, private equity is fucking stupid, doesn’t understand technology, doesn’t understand business, and by setting up its holdings with debt based on the assumption of unrealistic growth, they’ve created a crisis for both software companies and the greater tech industry.

On February 6, more than $17.7 billion of US tech company loans dropped to “distressed” trading levels (as in trading as if traders don’t believe they’ll get paid, per Bloomberg), growing the overall group of distressed tech loans to $46.9 billion, “dominated by firms in SaaS.” These firms included huge investments like Thoma Bravo’s Dayforce (which it purchased two days before this story ran for $12.3 billion) and Calabrio (which it acquired for “over” $1 billion in April 2021 and merged with Verint in November 2025).

This isn’t just about the shit they’ve bought, but the destruction of the concept of “value” in the tech industry writ large. “Value” was not based on revenues, or your product, or anything other than your ability to grow and, ideally, trap as many customers as possible, with the vague sense that there would always be infinitely more money every year to spend on software.

Revenue growth came from massive sales teams compensated with heavy commissions and yearly price increases, except things have begun to sour, with renewals now taking twice as long to complete, and overall SaaS revenue growth slowing for years.

To put it simply, much of the investment in software was based on the idea that software companies will always grow forever, and SaaS companies — which have “sticky” recurring revenues — would be the standard-bearer.

Private Equity And Venture Capital Have Driven A Valuation Crisis In The Tech Industry Based on Hype and Ignorance — And AI May Be Their Reckoning

When I got into the tech industry in 2008, I immediately became confused about the amount of unprofitable or unsustainable companies that were worth crazy amounts of money, and for the most part I’d get laughed at by reporters for being too cynical.

For the best part of 20 years, software startups have been seen as eternal growth-engines. All you had to do was find a product-market fit, get a few hundred customers locked in, up-sell them on new features and grow in perpetuity as you conquered a market. The idea was that you could just keep pumping them with cash, hire as many pre-sales (technical person who makes the sale), sales and customer experience (read: helpful person who also loves to tell you more stuff) people as you need to both retain customers and sell them as much stuff as you need.

Innovation was, as you’d expect, judged entirely by revenue growth and net revenue retention:

In practice, this sounds reasonable: what percentage of your revenue are you making year-over-year? The problem is that this is a very easy to game stat, especially if you’re using it to raise money, because you can move customer billing periods around to make sure that things all continue to look good. Even then, per research by Jacco van der Kooji and Dave Boyce, net revenue retention is dropping quarter over quarter.

The other problem is that the entire process of selling software has separated from the end-user, which means that products (and sales processes) are oriented around selling that software to the person responsible for buying it rather than those doomed to use it.

Per Nik Suresh’s Brainwash An Executive Today, in a conversation with the Chief Technology Officer of a company with over 10,000 people, who had asked if “data observability,” a thing that they did not (and would not need to, in their position) understand, was a problem, and whether Nik had heard of Monte Carlo. It turned out that the executive in question had no idea what Monte Carlo or data observability was, but because they’d heard about it on LinkedIn, it was now all they could think about.

This is the environment that private equity bought into — a seemingly-eternal growth engine with pliant customers desperate to spend money on a product that didn’t have to be good, just functional-enough. These people do not know what they are talking about or why they are buying these companies other than being able to mumble out shit like “ARR” and “NRR+” and “TAM” and “CAC” and “ARPA” in the right order to convince themselves that something is a good idea without ever thinking about what would happen if it wasn’t. This allowed them to stick to the “big picture,” meaning “numbers that I can look at rather than any practical experience in software development.”

While I guess the concept of private equity isn’t morally repugnant, its current form — which includes venture capital — has led the modern state of technology into the fucking toilet, combining an initial flux of viable businesses, frothy markets and zero interest rates making it deceptively easy to raise money to acquire and deploy capital, leading to brainless investing, the death of logical due diligence, and potentially ruinous consequences for everybody involved.

Private equity spent decades buying a little bit of just about everything, enriching the already-rich by engaging with the most vile elements of the Rot Economy’s growth-at-all-costs mindset. Its success is predicated on near-perpetual levels of liquidity and growth in both its holdings and the holdings of those who exist only to buy their stock, and on a tech and business media that doesn’t think too hard about the reality of the problems their companies claim to solve.

The reckoning that’s coming is one built specifically to target the ignorant hubris that made them rich.

Private equity has yet to be punished by its limited partners and banks for investing in zombie assets, allowing it to pile into the unprofitable data centers underpinning the AI bubble, meaning that companies like Apollo, Blue Owl and Blackstone — all of whom participated in the ugly $10.2 billion acquisition of Zendesk in 2022 (after it rejected another PE offer of $17 billion in 2021) that included $5 billion in debt — have all become heavily-leveraged in giant, ugly debt deals covering assets that are obsolete to useless in a few years.

Alongside the fumbling ignorance of private equity sits the $3 trillion private credit industry, an equally-putrid, growth-drunk, and poorly-informed industry run with the same lax attention to detail and Big Brain Number Models that can justify just about any investment they want. Their half-assed due diligence led to billions of dollars of loans being given to outright frauds like First Brands, Tricolor and PosiGen, and, to paraphrase JP Morgan’s Jamie Dimon, there are absolutely more fraudulent cockroaches waiting to emerge.

You may wonder why this matters, as all of this is private credit.

Well, they get their money from banks. Big banks. In fact, according to the Federal Reserve of Boston, about 14% ($300 billion) of large banks’ total loan commitments to non-banking financial institutions in 2023 went to private equity and private credit, with Moody’s pegging the number around $285 billion, with an additional $340 billion in unused-yet-committed cash waiting in the wings.

Oh, and they get their money from you. Pension funds are among some of the biggest backers of private credit companies, with the New York City Employees Retirement System and CalPERS increasing their investments.

Today, I’m going to teach you all about private equity, private credit, and why years of reframing “value” to mean “growth” may genuinely threaten the global banking system, as well as how effectively every company raises money. An entirely-different system exists for the wealthy to raise and deploy capital, one with flimsy due diligence, a genuine lack of basic industrial knowledge, and hundreds of billions of dollars of crap it can’t sell.

These people have been able to raise near-unlimited capital to do basically anything they want because there was always somebody stupid enough to buy whatever they were selling, and they have absolutely no plan for what happens when their system stops working.

They’ll loan to anyone or invest in anything that confirms their biases, and those biases are equal parts moronic and malevolent. Now they’re investing teachers’ pensions and insurance premiums in unprofitable and unsustainable data centers, all because they have no idea what a good investment actually looks like.

Welcome to the Hater’s Guide To Private Equity, or “The Stupidest Assholes In The Room.”