This week, something strange happened. Oracle, a company that had just missed on its earnings and revenue estimates, saw a more-than-39% single day bump in its stock, leading a massive market rally.

Why? Because it said its remaining performance obligations — contracts signed that its customers yet to pay — had increased by $317 billion from the previous quarter, with CNBC reporting at the time that this was likely part of Oracle and OpenAI's planned additional 4.5 gigawatts of data center capacity being built in the US.

Analysts fawned over Oracle — again, as it missed estimates — with TD Cowen's Derrick Wood saying it was a "momentous quarter" (again, it missed) and that these numbers were "really amazing to see," and Guggenheim Securities' John DiFucci said he was "blown away." Deutsche Bank's Brad Zelnick added that "[analysts] were all kind of in shock, in a very good way."

RPOs, while standard (and required) accounting practice and based on actual signed contracts, are being used by Oracle as a form of marketing. Plans change, contracts can be canceled (usually with a kill fee, but nevertheless), and, especially in this case, clients can either not have the money to pay or die for the very same reason they can't pay. In Oracle's case, it isn’t simply promising ridiculous growth, it is effectively saying it’ll become the dominant player in all cloud compute.

A day after Oracle's earnings and a pornographic day of market swings, the Wall Street Journal reported that OpenAI and Oracle had signed a $300 billion deal, starting in "2027," though the Journal neglected to say whether that was the year or Oracle’s FY2027 (which starts June 1 2026).

Oracle claims that it will make $18 billion in cloud infrastructure revenue in FY2026, $32 billion in FY2027, $73 billion in FY2028, $114 billion in FY2029, and $144 billion in FY2030. While all of this isn't necessarily OpenAI (as it adds up to $381 billion), it's fair to assume that the majority of it is.

This means — as the $300 billion of the $317 billion of new contracts added by Oracle, and assuming OpenAI makes up 78% of its cloud infrastructure revenue ($300 billion out of $381 billion) — that OpenAI intends to spend over $88 billion fucking dollars in compute by FY2029, and $110 billion dollars in compute, AKA nearly as much as Amazon Web Services makes in a year, in FY2030.

A sidenote on percentages, and how I'm going to talk about this going forward. If I'm honest, there's also a compelling argument that more of it is OpenAI. Who else is using this much compute? Who has agreed, and why?

In any case, if you trust Oracle and OpenAI, this is what you are believing:

- The AI compute industry will grow by, at the very least, 500% by 2030, to over $200 billion in annual revenue, and almost all of that growth will come from one company: OpenAI.

- That Oracle can successfully complete the data centers in question, and that said data centers will be operational in time to provide that compute.

- That OpenAI — a company with no plan for profitability — will be able to afford three hundred billion dollars spread over 2027, 2028, 2029, and 2030.

- Oracle will, at this point, become a dominant player in cloud compute, with $144 billion in cloud infrastructure revenue, and it will do so mostly from one customer.

- Oracle's cloud infrastructure revenue will increase by 700% — from $18 billion in FY2026 to $144 billion in FY2030. This represents a growth rate of 68.2% a year, again from one customer.

- Oracle will, by FY2028, be making more in cloud infrastructure (it projects to make $73 billion) than all of Google Cloud did in 2024 ($43 billion). And it’ll make it from one customer.

- That Oracle has more incoming revenue than Amazon, Google, and Microsoft, and will be making almost the entirety of that from one god damn customer.

I want to write something smart here, but I can't get away from saying that this is all phenomenally, astronomically, ridiculously stupid.

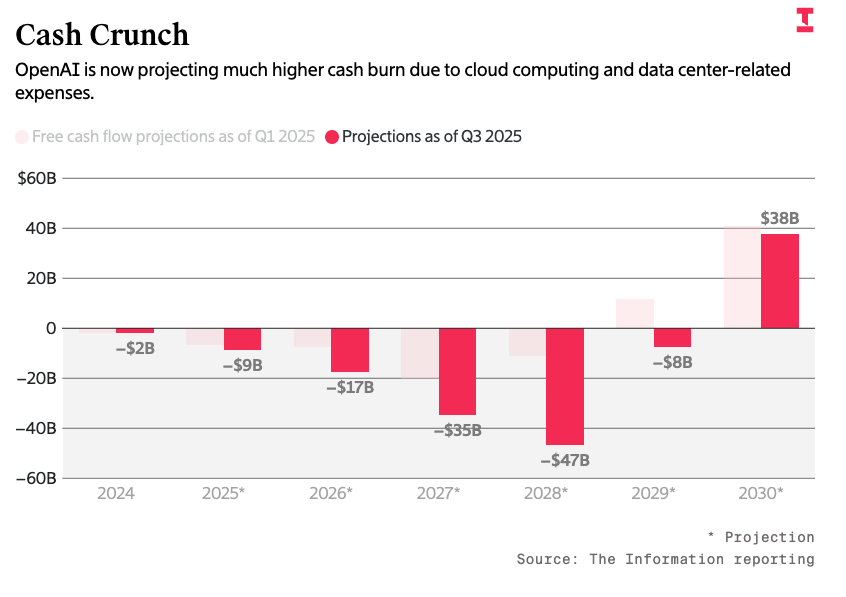

OpenAI, at present, has made about $6.26 billion in revenue this year, and it leaked a few days ago that it will burn $115 billion "through 2029," a statement that is obviously, patently false. Let's take a look at this chart from The Information:

A note on "free cash flow." Now, these numbers may look a little different because OpenAI is now leaking free cash flow instead of losses, likely because it lost $5 billion in 2024, which included $1 billion in losses from "research compute amortization," likely referring to spreading the cost of R&D out across several years, which means it already paid it. OpenAI also lost $700 million from its revenue share with Microsoft.

In any case, this is how OpenAI is likely getting its "negative $2 billion" number."

Personally, I don't like this as a means of judging this company's financial health, because it's very clear it’s using it to make its losses seem smaller than they are.

The Information also reports that OpenAI will, in totality, spend $350 billion in compute from here until 2030, but claims it’ll only spend $100 billion on compute in that year. If I'm honest, I believe it'll be more based on how much Oracle is projecting. OpenAI represents $300 billion of the $317 billion of new cloud infrastructure revenue it’ll from 2027 through 2030, which heavily suggests that OpenAI will be spending more like $140 billion in that year.

As I'll reveal in this piece, I believe OpenAI's actual burn is over $290 billion through 2029, and these leaks were intentional to muddy the waters around how much their actual costs would be.

There is no way a $116 billion burnrate from 2025 to 2029 includes these costs, and I am shocked that more people aren't doing the basic maths necessary to evaluate this company. The timing of the leak — which took place on September 5, 2025, five days before the Oracle deal was announced — always felt deeply suspicious, as it's unquestionably bad news...unless, of course, you are trying to undersell how bad your burnrate is.

I believe that OpenAI's leaked free cash flow projections intentionally leave out the Oracle contract as a means of avoiding scrutiny.

I refuse to let that happen.

So, even if OpenAI somehow had the money to pay for its compute — it won't, but it projects, according to The Information, that it’ll make one hundred billion dollars in 2028 — I'm not confident that Oracle will actually be able to build the capacity to deliver it.

Vantage Data Centers, the partner building the sites, will be taking on $38 billion of debt to build two sites in Texas and Wisconsin, only one of which has actually broken ground from what I can tell, and unless it has found a miracle formula that can grow data centers from nothing, I see no way that it can provide OpenAI with $70 billion or more of compute in FY2027.

Oracle and OpenAI are working together to artificially boost Oracle's stock based on a contract that is, from everything I can see, impossible for either party to fulfill.

The fact that this has led to such an egregious pump of Oracle's stock is an utter disgrace, and a sign that the markets and analysts are no longer representative of any rational understanding of a company's value.

Let me be abundantly clear: Oracle and OpenAI's deal says nothing about demand for GPU compute.

OpenAI is the largest user of compute in the entirety of the generative AI industry. Anthropic expects to burn $3 billion this year (so we can assume that its compute costs are $3 billion to $5 billion, Amazon is estimated to make $5 billion in AI revenue this year, so I think this is a fair assumption), and xAI burns through a billion dollars a month. CoreWeave expects about $5.3 billion of revenue in 2025, and per The Information Lambda, another AI compute company, made more than $250 million in the first half of 2025. If we assume that all of these companies were active revenue participants (we shouldn't, as xAI mostly handles its own infrastructure), I estimate the global compute market is about $40 billion in totality, at a time when AI adoption is trending downward in large companies according to Apollo's Torsten Sløk.

And yes, Nebius signed a $17.4 billion, four-year-long deal with Microsoft, but Nebius now has to raise $3 billion to build the capacity to acquire "additional compute power and hardware, [secure] land plots with reliable providers, and [expand] its data center footprint," because Nebius, much like CoreWeave, and, much like Oracle, doesn't have the compute to service these contracts.

All three have seen a 30% bump in their stock in the last week.

In any case, today I'm going to sit down and walk you through the many ways in which the Oracle and OpenAI deal is impossible to fulfill for either party. OpenAI is projecting fantastical growth in an industry that's already begun to contract, and Oracle has yet to even start building the data centers necessary to provide the compute that OpenAI allegedly needs.