Have you ever looked at something too long and felt like you were sort of seeing through it? Has anybody actually looked at a company this much in a way that wasn’t some sort of obsequious profile of a person who worked there? I don’t mean this as a way to fish for compliments — this experience is just so peculiar, because when you look at them hard enough, you begin to wonder why everybody isn’t just screaming all the time.

Yet I really do enjoy it. When you push aside all the marketing and the interviews and all that and stare at what a company actually does and what its users and employees say, you really get a feel of the guts of a company. I’m enjoying it. The Hater’s Guides are a lot of fun, and I’m learning all sorts of things about the ways in which companies try to hide their nasty little accidents and proclivities.

Today, I focus on one of the largest.

In the last year I’ve spoken to over a hundred different tech workers, and the ones I hear most consistently from are the current and former victims of Microsoft, a company with a culture in decline, in large part thanks to its obsession with AI. Every single person I talk to about this company has venom on their tongue, whether they’re a regular user of Microsoft Teams or somebody who was unfortunate to work at the company any time in the last decade.

Microsoft exists as a kind of dark presence over business software and digital infrastructure. You inevitably have to interact with one of its products — maybe it’s because somebody you work with uses Teams, maybe it’s because you’re forced to use SharePoint, or perhaps you’re suffering at the hands of PowerBI — because Microsoft is the king of software sales. It exists entirely to seep into the veins of an organization and force every computer to use Microsoft 365, or sit on effectively every PC you use, forcing you to interact with some sort of branded content every time you open your start menu.

This is a direct results of the aggressive monopolies that Microsoft built over effectively every aspect of using the computer, starting by throwing its weight around in the 80s to crowd out potential competitors to MS-DOS and eventually moving into everything including cloud compute, cloud storage, business analytics, video editing, and console gaming, and I’m barely a third through the list of products.

Microsoft uses its money to move into new markets, uses aggressive sales to build long-term contracts with organizations, and then lets its products fester until it’s forced to make them better before everybody leaves, with the best example being the recent performance-focused move to “rebuild trust in Windows” in response to the upcoming launch of Valve’s competitor to the Xbox (and Windows gaming in general), the Steam Machine.

Microsoft is a company known for two things: scale and mediocrity. It’s everywhere, its products range from “okay” to “annoying,” and virtually every one of its products is a clone of something else.

And nowhere is that mediocrity more obvious than in its CEO.

Since taking over in 2014, CEO Satya Nadella has steered this company out of the darkness caused by aggressive possible chair-thrower Steve Ballmer, transforming from the evils of stack ranking to encouraging a “growth mindset” where you “believe your most basic abilities can be developed through dedication and hard work.” Workers are encouraged to be “learn-it-alls” rather than “know-it-alls,” all part of a weird cult-like pseudo-psychology that doesn’t really ring true if you actually work at the company.

Nadella sells himself as a calm, thoughtful and peaceful man, yet in reality he’s one of the most merciless layoff hogs in known history. He laid off 18,000 people in 2014 months after becoming CEO, 7,800 people in 2015, 4,700 people in 2016, 3,000 people in 2017, “hundreds” of people in 2018, took a break in 2019, every single one of the workers in its physical stores in 2020 along with everybody who worked at MSN, took a break in 2021, 1,000 people in 2022, 16,000 people in 2023, 15,000 people in 2024 and 15,000 people in 2025.

Despite calling for a “referendum on capitalism” in 2020 and suggesting companies “grade themselves” on the wider economic benefits they bring to society, Nadella has overseen an historic surge in Microsoft’s revenues — from around $83 billion a year when he joined in 2014 to around $300 billion on a trailing 12-month basis — while acting in a way that’s callously indifferent to both employees and customers alike.

At the same time, Nadella has overseen Microsoft’s transformation from an asset-light software monopolist that most customers barely tolerate to an asset-heavy behemoth that feeds its own margins into GPUs that only lose it money. And it’s that transformation that is starting to concern investors, and raises the question of whether Microsoft is heading towards a painful crash.

You see, Microsoft is currently trying to pull a fast one on everybody, claiming that its investments in AI are somehow paying off despite the fact that it stopped reporting AI revenue in the first quarter of 2025. In reality, the one segment where it would matter — Microsoft Azure, Microsoft’s cloud platform where the actual AI services are sold — is stagnant, all while Redmond funnels virtually every dollar of revenue directly into more GPUs.

Intelligent Cloud also represents around 40% of Microsoft’s total revenue, and has done so consistently since FY2022. Azure sits within Microsoft's Intelligent Cloud segment, along with server products and enterprise support.

For the sake of clarity, here’s how Microsoft describes Intelligent Cloud in its latest end-of-year K-10 filing:

Our Intelligent Cloud segment consists of our public, private, and hybrid server products and cloud services that power modern business and developers. This segment primarily comprises:

- Server products and cloud services, including Azure and other cloud services, comprising cloud and AI consumption-based services, GitHub cloud services, Nuance Healthcare cloud services, virtual desktop offerings, and other cloud services; and Server products, comprising SQL Server, Windows Server, Visual Studio, System Center, related Client Access Licenses (“CALs”), and other on-premises offerings.

- Enterprise and partner services, including Enterprise Support Services, Industry Solutions, Nuance professional services, Microsoft Partner Network, and Learning Experience.

It’s a big, diverse thing — and Microsoft doesn’t really break things down further from here — but Microsoft makes it clear in several places that Azure is the main revenue driver in this fairly diverse business segment.

Some bright spark is going to tell me that Microsoft said it has 15 million paid 365 Copilot subscribers (which, I add, sits under its Productivity and Business Processes segment), with reporters specifically saying these were corporate seats, a fact I dispute, because this is the quote from Microsoft’s latest conference call around earnings:

We saw accelerating seat growth quarter-over-quarter and now have 15 million paid Microsoft 365 Copilot seats, and multiples more enterprise Chat users.

At no point does Microsoft say “corporate seat” or “business seat.” “Enterprise Copilot Chat” is a free addition to multiple different Microsoft 365 products, and Microsoft 365 Copilot could also refer to Microsoft’s $18 to $21-a-month addition to Copilot Business, as well as Microsoft’s enterprise $30-a-month plans. And remember: Microsoft regularly does discounts through its resellers to bulk up these numbers.

As an aside: If you are anything to do with the design of Microsoft’s investor relations portal, you are a monster. Your site sucks. Forcing me to use your horrible version of Microsoft Word in a browser made this newsletter take way longer. Every time I want to find something on it I have to click a box and click find and wait for your terrible little web app to sleepily bumble through your 10-Ks.

If this is a deliberate attempt to make the process more arduous, know that no amount of encumbrance will stop me from going through your earnings statements, unless you have Satya Nadella read them. I’d rather drink hemlock than hear another minute of that man speak after his interview from Davos. He has an answer that’s five and a half minutes long that feels like sustaining a concussion.

Microsoft Is Wasting Its Money On AI — And Using It To Paper Over The Flagging Growth Of Azure

When Nadella took over, Microsoft had around $11.7 billion in PP&E (property, plant, and equipment). A little over a decade later, that number has ballooned to $261 billion, with the vast majority added since 2020 (when Microsoft’s PP&E sat around $41 billion).

Also, as a reminder: Jensen Huang has made it clear that GPUs are going to be upgraded on a yearly cycle, guaranteeing that Microsoft’s armies of GPUs regularly hurtle toward obsolescence. Microsoft, like every big tech company, has played silly games with how it depreciates assets, extending the “useful life” of all GPUs so that they depreciate over six years, rather than four.

And while someone less acquainted with corporate accounting might assume that this move is a prudent, fiscally-conscious tactic to reduce spending by using assets for longer, and stretching the intervals between their replacements, in reality it’s a handy tactic to disguise the cost of Microsoft’s profligate spending on the balance sheet.

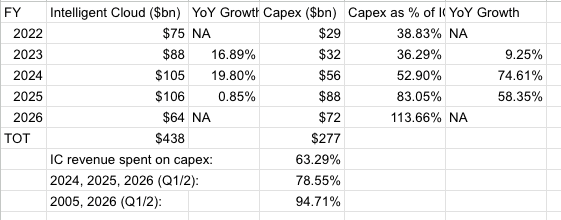

You might be forgiven for thinking that all of this investment was necessary to grow Azure, which is clearly the most important part of Microsoft’s Intelligent Cloud segment. In Q2 FY2020, Intelligent Cloud revenue sat at $11.9 billion on PP&E of around $40 billion, and as of Microsoft’s last quarter, Intelligent Cloud revenue sat at around $32.9 billion on PP&E that has increased by over 650%.

Good, right? Well, not really. Let’s compare Microsoft’s Intelligent Cloud revenue from the last five years:

In the last five years, Microsoft has gone from spending 38% of its Intelligent Cloud revenue on capex to nearly every penny (over 94%) of it in the last six quarters, at the same time in two and a half years that Intelligent Cloud has failed to show any growth.

An important note: If you look at Microsoft’s 2025 K-10, you’ll notice that it lists the Intelligent Cloud revenue for 2024 as $87.4bn — not, as the above image shows, $105bn.

If you look at the 2024 K-10, you’ll see that Intelligent Cloud revenues are, in fact, $105bn. So, what gives?

Essentially, before publishing the 2025 K-10, Microsoft decided to rejig which part of its operations fall into which particular segments, and as a result, it had to recalculate revenues for the previous year. Having read and re-read the K-10, I’m not fully certain which bits of the company were recast.

It does mention Microsoft 365, although I don’t see how that would fall under Intelligent Cloud — unless we’re talking about things like Sharepoint, perhaps. I’m at a loss. It’s incredibly strange.

Things, I’m afraid, get worse. Microsoft announced in July 2025 — the end of its 2025 fiscal year— that Azure made $75 billion in revenue in FY2025. This was, as the previous link notes, the first time that Microsoft actually broke down how much Azure actually made, having previously simply lumped it in with the rest of the Intelligent Cloud segment.

I’m not sure what to read from that, but it’s still not good. meaning that Microsoft spent every single penny of its Azure revenue from that fiscal year on capital expenditures of $88 billion and then some, a little under 117% of all Azure revenue to be precise. If we assume Azure regularly represents 71% of Intelligent Cloud revenue, Microsoft has been spending anywhere from half to three-quarters of Azure’s revenue on capex.

To simplify: Microsoft is spending lots of money to build out capacity on Microsoft Azure (as part of Intelligent Cloud), and growth of capex is massively outpacing the meager growth that it’s meant to be creating.

You know what’s also been growing? Microsoft’s depreciation charges, which grew from $2.7 billion in the beginning of 2023 to $9.1 billion in Q2 FY2026, though I will add that they dropped from $13 billion in Q1 FY2026, and if I’m honest, I have no idea why! Nevertheless, depreciation continues to erode Microsoft’s on-paper profits, growing (much like capex, as the two are connected!) at a much-faster rate than any investment in Azure or Intelligent Cloud.

But worry not, traveler! Microsoft “beat” on earnings last quarter, making a whopping $38.46 billion in net income…with $9.97 billion of that coming from recapitalizing its stake in OpenAI. Similarly, Microsoft has started bulking up its Remaining Performance Obligations. See if you can spot the difference between Q1 and Q2 FY26, emphasis mine:

Q1FY26:

Revenue allocated to remaining performance obligations, which includes unearned revenue and amounts that will be invoiced and recognized as revenue in future periods, was $398 billion as of September 30, 2025, of which $392 billion is related to the commercial portion of revenue. We expect to recognize approximately 40% of our total company remaining performance obligation revenue over the next 12 months and the remainder thereafter.

Q2FY26:

Revenue allocated to remaining performance obligations related to the commercial portion of revenue was $625 billion as of December 31, 2025, with a weighted average duration of approximately 2.5 years. We expect to recognize approximately 25% of both our total company remaining performance obligation revenue and commercial remaining performance obligation revenue over the next 12 months and the remainder thereafter

So, let’s just lay it out:

- Q1: $398 billion of RPOs, 40% within 12 months, $159.2 billion in upcoming revenue.

- Q2: $625 billion of RPOs, 25% within 12 months, $156.25 billion in upcoming revenue.

…Microsoft’s upcoming revenue dropped between quarters as every single expenditure increased, despite adding over $200 billion in revenue from OpenAI. A “weighted average duration” of 2.5 years somehow reduced Microsoft’s RPOs.

But let’s be fair and jump back to Q4 FY2025…

Revenue allocated to remaining performance obligations, which includes unearned revenue and amounts that will be invoiced and recognized as revenue in future periods, was $375 billion as of June 30, 2025, of which $368 billion is related to the commercial portion of revenue. We expect to recognize approximately 40% of our total company remaining performance obligation revenue over the next 12 months and the remainder thereafter.

40% of $375 billion is $150 billion. Q3 FY25? 40% on $321 billion, or $128.4 billion. Q2 FY25? $304 billion, 40%, or $121.6 billion.

It appears that Microsoft’s revenue is stagnating, even with the supposed additions of $250 billion in spend from OpenAI and $30 billion from Anthropic, the latter of which was announced in November but doesn’t appear to have manifested in these RPOs at all.

In simpler terms, OpenAI and Anthropic do not appear to be spending more as a result of any recent deals, and if they are, that money isn’t arriving for over a year.

Much like the rest of AI, every deal with these companies appears to be entirely on paper, likely because OpenAI will burn at least $115 billion by 2029, and Anthropic upwards of $30 billion by 2028, when it mysteriously becomes profitable two years before OpenAI “does so” in 2030.

These numbers are, of course, total bullshit. Neither company can afford even $20 billion of annual cloud spend, let alone multiple tens of billions a year, and that’s before you get to OpenAI’s $300 billion deal with Oracle that everybody has realized (as I did in September) requires Oracle to serve non-existent compute to OpenAI and be paid hundreds of billions of dollars that, helpfully, also don’t exist.

Yet for Microsoft, the problems are a little more existential.

Microsoft Is A Decaying Empire That Bet The Future On Making In Excess Of $500 Billion In New Revenue Within The Next 4 To 6 Years From AI — And It Hasn’t Made A Dime In Profit Yet

Last year, I calculated that big tech needed $2 trillion in new revenue by 2030 or investments in AI were a loss, and if anything, I think I slightly underestimated the scale of the problem.

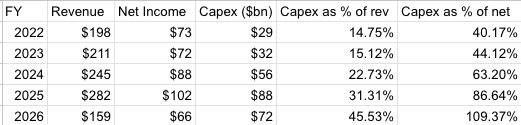

As of the end of its most recent fiscal quarter, Microsoft has spent $277 billion or so in capital expenditures since the beginning of FY2022, with the majority of them ($216 billion) happening since the beginning of FY2024. Capex has ballooned to the size of 45.5% of Microsoft’s FY26 revenue so far — and over 109% of its net income.

This is a fucking disaster. While net income is continuing to grow, it (much like every other financial metric) is being vastly outpaced by capital expenditures, none of which can be remotely tied to profits, as every sign suggests that generative AI only loses money.

While AI boosters will try and come up with complex explanations as to why this is somehow alright, Microsoft’s problem is fairly simple: it’s now spending 45% of its revenues to build out data centers filled with painfully expensive GPUs that do not appear to be significantly contributing to overall revenue, and appear to have negative margins.

Those same AI boosters will point at the growth of Intelligent Cloud as proof, so let’s do a thought experiment (even though they are wrong): if Intelligent Cloud’s segment growth is a result of AI compute, then the cost of revenue has vastly increased, and the only reason we’re not seeing it is that the increased costs are hitting depreciation first.

You see, Intelligent Cloud is stalling, and while it might be up by 8.8% on an annualized basis (if we assume each quarter of the year will be around $30 billion, that makes $120 billion, so about an 8.8% year-over-year increase from $106 billion), that’s come at the cost of a massive increase in capex (from $88 billion for FY2025 to $72 billion for the first two quarters of FY2026), and gross margins that have deteriorated from 69.89% in Q3 FY2024 to 68.59% in FY2026 Q2, and while operating margins are up, that’s likely due to Microsoft’s increasing use of contract workers and increased recruitment in cheaper labor markets.

And as I’ll reveal later, Microsoft has used OpenAI’s billions in inference spend to cover up the collapse of the growth of the Intelligent Cloud segment. OpenAI’s inference spend now represents around 10% of Azure’s revenue.

Microsoft, as I discussed a few weeks ago, is in a bind. It keeps buying GPUs, all while waiting for the GPUs it already has to start generating revenue, and every time a new GPU comes online, its depreciation balloons. Capex for GPUs began in seriousness in Q1 FY2023 following October’s shipments of NVIDIA’s H100 GPUs, with reports saying that Microsoft bought 150,000 H100s in 2023 (around $4 billion at $27,000 each) and 485,000 H100s in 2024 ($13 billion). These GPUs are yet to provide much meaningful revenue, let alone any kind of profit, with reports suggesting (based on Oracle leaks) that the gross margins of H100s are around 26% and A100s (an older generation launched in 2020) are 9%, for which the technical term is “dogshit.” Somewhere within that pile of capex also lies orders for H200 GPUs, and as of 2024, likely NVIDIA’s B100 (and maybe B200) Blackwell GPUs too.

You may also notice that those GPU expenses are only some portion of Microsoft’s capex, and the reason is because Microsoft spends billions on finance leases and construction costs. What this means in practical terms is that some of this money is going to GPUs that are obsolete in 6 years, some of it’s going to paying somebody else to lease physical space, and some of it is going into building a bunch of data centers that are only useful for putting GPUs in.

And none of this bullshit is really helping the bottom line! Microsoft’s More Personal Computing segment — including Windows, Xbox, Microsoft 365 Consumer, and Bing — has become an increasingly-smaller part of revenue, representing in the latest quarter a mere 17.64% of Microsoft’s revenue in FY26 so far, down from 30.25% a mere four years ago.

We are witnessing the consequences of hubris — those of a monopolist that chased out any real value creators from the organization, replacing them with an increasingly-annoying cadre of Business Idiots like career loser Jay Parikh and scummy, abusive timewaster Mustafa Suleyman.

Satya Nadella took over Microsoft with the intention of fixing its culture, only to replace the aggressive, loudmouthed Ballmer brand with a poisonous, passive aggressive business mantra of “you’ve always got to do more with less.”

Today, I’m going to walk you through the rotting halls of Redmond’s largest son, a bumbling conga line of different businesses that all work exactly as well as Microsoft can get away with.

Welcome to The Hater’s Guide To Microsoft, or Instilling The Oaf Mindset.