Imagine you are talking to a regular human being. That human being has no experience with the blockchain, cryptocurrency, or anything like that. You open your mouth and say to them, “a multi-billion dollar cryptocurrency company has apologized to users after its sale of “metaverse land” sparked a frenzy that temporarily brought down the Ethereum cryptocurrency.”

They ask you a simple question - “what in the world are you talking about?” and you lash out, failing the Voight-Kampff test.

You see, this entire situation defies reality. Every time I have read about this story, I have felt a kind of pain in my soul - the feeling that I am watching the end of some part of society or the birth of something else, something very dark and sad.

To explain in simple terms, Yuga Labs, the creators of the Bored Ape Yacht Club NFT (a collection of thousands of unique, algorithmically-generated digital tokens of pictures of apes that are worth lots of money for absolutely no reason), decided to sell 55,000 plots of “land” (NFTs of land in digital space) in a game called “Otherside,” which will ostensibly take place on the Ethereum decentralized blockchain.

A note on how this chain works: every “transaction” you do on the Ethereum blockchain (for example, minting (creating) a token, or withdrawing said token) costs a certain amount of Ethereum - which is currently around $2844 - to send it. This price increases or decreases based on network congestion, meaning that when lots of people want to do something on the Ethereum network, it becomes quite expensive. It’s also worth noting that if you’d like to give a transaction priority on the network, you can pay more Ethereum to make it go faster. This is the nature of a decentralized network.

As expected, these pieces of land were extremely popular and could only be bought using 305 “ApeCoin,” a separate token created by Yuga Labs based on your ownership of Bored Apes. As a result, the Ethereum network became extremely expensive to transact on. The average fees entered the hundreds of dollars, with The Guardian citing one particular person spending thousands of dollars in transaction fees to secure their “land.”

To be clear, if you did not have thousands of dollars, you could not participate. One ApeCoin is currently worth $14.90, which is less than they were worth during the sale. Even if you had the sufficient ApeCoins - thousands of dollars’ worth - you also had to pony up whatever the costs were on the Ethereum network to potentially purchase one, as transactions can fail - and there are no refunds for failed transactions. However, Yuga Labs has insisted they will refund lost fees. I’ll believe it when I see it.

This, my friends, is the beautiful, utilitarian cryptocurrency future - a literal kleptocracy where the richest people have the most access to the means to get even richer and where those who have the least risk what little they have in their desperation to join the wealthy. Nobody is buying this land to “participate in the metaverse” - they want the ability to buy and hold a speculative asset that will potentially increase in value.

What’s important to remember is that this situation also completely demolished the rest of the Ethereum network. If you wanted to do anything - yes, including the artists that allegedly make money selling stuff on OpenSea, which also runs on the Ethereum network - you either had to pay the exorbitant fees or wait until said fees were lower. To be clear about what this means, if you were the mythical artist making their money selling unique NFT artwork, you would be paying these fees to list something on OpenSea, withdraw the proceeds of a sale, or do anything with your artwork.

Naturally, this has led to Yuga Labs saying that they might need their own blockchain, sort of like how you get a cat a litter box for when it wants to go to the bathroom rather than teaching it to use yours like Charles Mingus. All signs point to this blockchain being extremely well-built, especially because the contract for Otherside land was so poorly-optimized that it wasted $100 million in Ethereum fees.

Apentropy

To summarize, the Ethereum network - one of the top blockchains and one specifically known for running software called smart contracts - became completely unusable to anyone except those who could burn thousands of dollars, all because too many people wanted to use it.

Cryptocurrency is (allegedly) about giving access to wealth and “the future” to everybody, and yet Ethereum is at its very core the single least inclusive or democratic system around. Those who control the network are those who can afford expensive mining gear, real estate, and raw power to mine Ethereum. The more people who use it, the more expensive it gets, naturally excluding more and more people until the ones who participate are either already rich or experiencing financial ruin with every bit of information exchanged.

The theory, of course, is that the higher transaction costs will dissuade users from participating until they come down, something that makes sense as long as you assume that human beings operate logically. However, since the cryptocurrency industry employs deceptive, quasi-religious tactics to keep people in the system, people feel the need to keep feeding the beast because participation is how you prove you’re “part of the community.” In fact, many people say that the transaction fees are “worth it” because…of…innovation? I am honestly not sure.

Yes, there are other, faster chains, like Solana, a network that has completely shut down 7 times in 2022, or Polygon, which also had downtime in 2022 due to the developers pushing a hotfix for a bug, a thing that definitely makes sense in a decentralized network. You have other options in cryptocurrency, but the biggest projects are going to appear on the networks with the largest amounts of suckers users to sell to.

And all of that traffic may have just been desperation by NFT zealots to try and find a way to make some money in a dying industry. Outside of selling pieces of land that I assume you can make your digital apes live in, NFT sales are absolutely cratering, reports the Wall Street Journal:

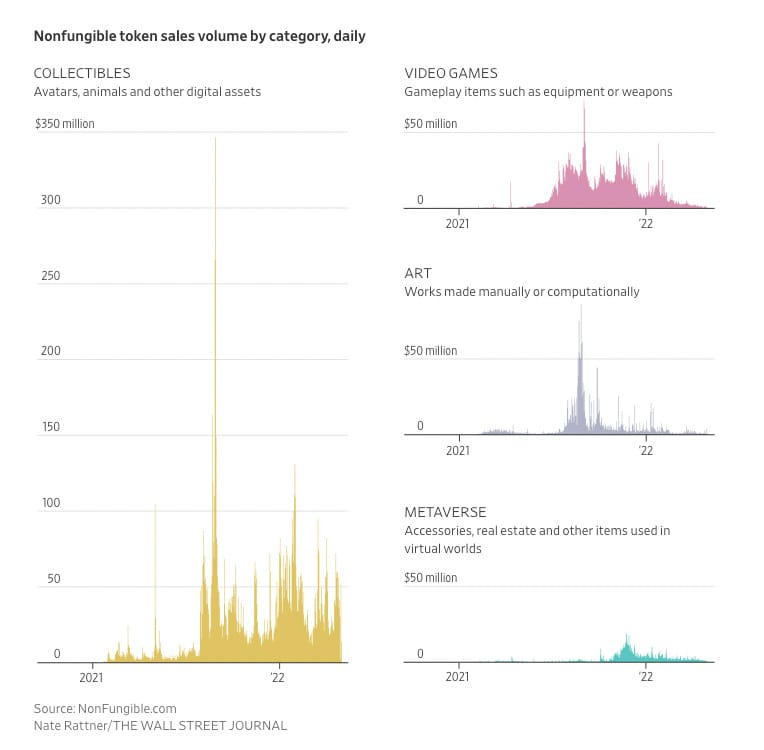

The sale of nonfungible tokens, or NFTs, fell to a daily average of about 19,000 this week, a 92% decline from a peak of about 225,000 in September, according to the data website NonFungible.

The number of active wallets in the NFT market fell 88% to about 14,000 last week from a high of 119,000 in November. NFTs are bitcoin-like digital tokens that act like a certificate of ownership that live on a blockchain.

…

That lack of interest isn’t unique. Interest in NFTs measured by the number of searches for the term peaked in January, according to Google Trends, and has fallen roughly 80% since then.

The imbalance between supply and demand is also hurting the NFT market. There are about five NFTs for every buyer, according to data from analytics firm Chainalysis. As of the end of April, there have been 9.2 million NFTs sold, which were bought by 1.8 million people, the firm said.

As I’ve written before, NFTs (as with most of the cryptocurrency industry) are supported by a thick layer of religious zealotry that exists in place of a real purpose or utility. As a result, there is very little that seems to hold this industry together other than hype and speculation - as the Journal has reported (see below), the pops and drops within the industry seem to be coupled together. In fact, the more utility an NFT has, the less likely it seems to really take off - almost as if the interest in the industry is entirely based on trying to flip them for a quick buck.

It might be tempting to assume that NFT marketplace OpenSea’s record trading volume on the day of the Otherside sale was an indicator that the industry isn’t dead, but in my mind it proves exactly how small the industry is, despite how much money flows through it. This wasn’t money pouring into desperate artists that finally had a way to get an income - it went to the miners running the Ethereum network, OpenSea’s transaction fees, and in and out of the hands of people that could afford to pay thousands of dollars to guarantee they’d own a piece of digital land in a “metaverse” that as of now has no real shape or form.

If anything, this situation has shown how utterly broken everything surrounding cryptocurrency is. This is the equivalent of a particularly popular concert sale on Ticketmaster bringing Amazon Web Services to its knees, all to enrich a small group of rich guys who didn’t want their identities published. Despite the vast amount of money that Yuga Labs raised, the rest of the NFT industry is tumbling downwards - their success has not caused the value of other assets to increase along with it, nor has it legitimized anything to do with the “metaverse” or NFTs. In fact, as of writing the floor of Otherside’s “Otherdeed” NFTs is 3.83 Ethereum - roughly double what the pieces of land cost, which is cool but also not a sign of the market being desperate to acquire them. Sales volume is also trending downward, (meaning that less people are trading the pieces of land), from 114,000 Eth on 5/1 to 20,000 Eth on 5/3.

And, on some level, people may have realized that these are not real things that connect to a tangible benefit of any kind. Despite the eye-watering amounts of money being exchanged, Otherside itself sounds like every single crypto vaporware product I’ve ever seen:

Otherside is a gamified, interoperable metaverse currently under development. The game blends mechanics from massively multiplayer online role playing games (MMORPGs) and web3-enabled virtual worlds. Think of it as a metaRPG where the players own the world, your NFTs can become playable characters, and thousands can play together in real time.

Yuga Labs has had to prove nothing to raise this money, other than creating vague collateral about what you might be able to do in “Otherside.” The raw details suggest there will be multiple game-related tokens (Anima, Ore, Shard and Root) that sound alarmingly similar to the many ones associated with Axie Infinity, and that it is something involving land where you can “get treasures” that you “own.”

Yuga has become the ultimate libertarian company, one that actively exploits both the holders of Bored Apes (from the royalties of sales of said apes) and those desperate to be involved in “the future,” even if said future is so poorly-described that it’s impossible to imagine. They are proof of my larger thesis about cryptocurrency - that this is pure libertarianism, where the total lack of rules allows millionaires and billionaires to exploit infrastructure in any way they see fit, even if it involves causing meaningful harm to others. And in this wonderful, democratic, open future, the most wealthy participants are the Andreessen Horowitz-backed founders of a company that does nothing other than offering people speculative investments based on the loosest possible definition of value.

The beauty of a decentralized, lawless network is that anyone can do whatever they want on it - including but not limited to making it fiscally impossible to operate on for the vast majority of people. And Yuga Labs is absolutely aware of what they’re doing - charging thousands of dollars for non-existent land in a non-existent game that will come out based on a non-existent timeline, sold to people that claim they want to disempower the “elites” while trying to create enough wealth to become one of them.