Every so often, I get a weird gut instinct, a sort of white noise of nausea that says something bad is going to happen, long before my logical brain actually realizes what I’m worried about or what’s going to happen. It’s happened in late 2019, and a few months ago, and I am currently feeling it right now as I read the surprisingly negative press around Bitcoin’s return to $23,500.

I also apologize, because I am about to go a little deep in the weeds. But hey, the newsletter’s free, right?

Yesterday, miners moved around $300 million of Bitcoin out of their wallets, and, according to CNBC, this is the largest dumping of BTC from the mining community since January 2021. As I’ve discussed before, crypto lender Voyager shuttered withdrawals, and then filed for bankruptcy, and then claimed that they would honor withdrawals of $350 million in cash held by its custodian bank Metropolitan, which is possibly the only good news that will come out of Voyager for the rest of time. Celsius, another lender, also froze withdrawals last week, then filed for bankruptcy and revealed a $1.2 billion hole in their balance sheet, while also claiming that they had “$600 million in CEL token,” the native token of Celsius, despite the fact that the market cap of the CEL token on July 12 was $170.3m (it is currently, puzzlingly, just over $188 million as I write this). Customers are all-but-certain to have lost their money, and Celsius’ lawyers are claiming that users “gave up legal rights to their BTC by using the platform.”

Meanwhile, American crypto giant Coinbase suspended their affiliate marketing program which gave people a whopping two dollars per new user, which suggests that Coinbase, a company which effectively prints its own money, may not have enough of it. Garbage Day’s Ryan Broderick (who I believe is the son of actor Matthew Broderick) put it depressingly well:

I saw multiple tweets over the weekend from big crypto influencers advising users to get their money out of Coinbase just in case the affiliate marketing shutdown was a sign of something worse coming over the horizon. Which led to Coinbase execs taking to Twitter over the weekend to combat rumors that the company might have some kind of liquidity issue. CEO Brian Armstrong said the end of the affiliate marketing program was actually because they’re doing too well. Armstrong’s very believable tweets about a very normal problem all kinds of companies have did not stop almost $250 million worth of stablecoins from leaving Coinbase, according to CryptoQuant. What that means in normal English is that a lot of people who were storing their money on Coinbase are no longer storing their money on Coinbase.

I actually want to take this argument a step further, and say that while I don’t think Coinbase will become insolvent, I no longer know for sure that they will not. At the end of June, Coinbase announced that they would combine the order books of USDC - a stablecoin that is meant to equal one US dollar - and the order books of actual, real US dollars as of July 13. They claimed that this would “create a better, more seamless trading experience with deeper liquidity for USDC and USD,” and I would like to ask a question: what?

You see, a real US dollar is a real US dollar. If I had 8 casino chips of a dollar each and 8 US dollars, those casino chips would only be useful as long as the casino in question operated. If I took them to Wells Fargo, they would look at me and say “sir, this is not 8 dollars, these are casino chips,” and they would not listen if I told them that I was, in fact, helping them create a more seamless banking experience with more liquidity for the US dollar.

Sidebar: If you’re relatively new to cryptocurrency, a stablecoin is a token that is meant to equal one real currency. USDC is a stablecoin for the US Dollar. They keep reserves so that when somebody wants to sell one USDC, they can receive one real US dollar in return.

The reason they do this is it makes a dollar portable - you can send one “dollar” in the form of USDC to an exchange, or into a crypto project, or to someone who claims to be your grandchild, all within a matter of seconds.

However, to be clear, one USDC is not a dollar. There are places that might recognize it as valued as one dollar, but until you have exchanged it for a dollar (at Coinbase or another exchange), it is still a token.

If the point of a USD order book - the place where one gets dollars from - is to acquire a US dollar, then combining said order book with a token that is meant to mean a US dollar does not feel right, and suggests to me that Coinbase has a liquidity crisis brewing that nobody is worried about. There is no reason to combine these order books unless you have a deficiency of either USDC or real US dollars, and I would wager that they’re running low on the one that actually exists.

At the beginning of July, crypto investment firm Robert Ventures CEO Joe Robert wrote a controversial piece considering whether USDC was on the brink of collapse, based partially on a Twitter thread breaking down Circle (the company that handles USDC)’s SPAC IPO:

A Twitter thread by @CryptoInsider23 says Circle is constantly losing money since the company has been raising money twice per year for the last years to pay for the ~5% incentives they offered.

According to Gerald Davidson’s (@CryptoInsider23) analysis on Twitter, Circle has already lost $500 million in the first quarter of 2022 and is on track to losing a total of $1.5 billion in the year.

And theoretically, USDC is now lent to high-risk lenders, such as Genesis, BlockFi, Celsius, Galaxy, Alameda, and 3AC. If this list is accurate, it comprises the companies mentioned at the beginning of our newsletter, which already collapsed or are about to do so.

The thread, while a little out there, suggests that Circle loses money maintaining the value of the USDC stablecoin, and warns of a “hole” of $3-$5 billion and risky loans - though it’s not obvious if he’s suggesting Circle made the loans or whether the loans were simply made in USDC. Does this suggest there’s an “imminent collapse”? No. But it certainly makes me think that something stinks.

Circle has, of course, claimed that everything is just great, and that they have total reserves of $55.7 billion - a whole $700 million higher than the $55 billion of USDC tokens in circulation. Their full asset breakdown shows $42.1 billion held in U.S. treasury bonds, and another $13.6 billion in cash, which is nice…until you remember that banks generally keep 10% of reserves on hand, as opposed to just over 1% in the case of USDC.

Circle is not a bank (they’re a registrered financial services company), but has hinted that they will apply to be one in the future. Nevertheless, they hold deposits, offer yields, and many other bank-adjacent infrastructure products, and also operate as a faux-Federal Reserve for the USDC stablecoin along with Coinbase as part of the Centre Consortium. They want to go public in Q4 of this year.

What bothers me about Circle is how they make money, based on their investor deck from June of last year. Let’s start with a few of the risk factors (Note: risk factors are standard for investor presentations like these):

- “If USDC does not grow as we expect, our business, operating results, and financial condition could be adversely affected.”

- “Issuing and redeeming USDC from our platform involve (sic?) risks, which could result in loss of customer assets, customer disputes and other liabilities, which could adversely impact our business.”

- “Our operating results from the yield service product may fluctuate due to market forces out of our control that impact demand to borrow cryptocurrency or stablecoins.”

- “We and our yield product customers are exposed to the credit risk of Genesis,” and yes, that would be the same Genesis that loaned Three Arrows Capital $2.3 billion.

- “Our consolidated balance sheets may not contain sufficient amounts or types of regulatory capital to meet the changing requirements of our various regulators worldwide, which could adversely affect our business, operating results, and financial condition.”

Wait, what was that last thing? That thing about your balance sheets not containing the amounts or types of regulatory capital for regulators? While this could be a case of covering one’s ass, one has to wonder what “consolidated bank sheets” and “not containing something” could combine to mean for the current state of Circle. USDC funds are held with a custodian bank, meaning that theoretically, USDC funds are safe, but that the company running it and maintaining its value may not be.

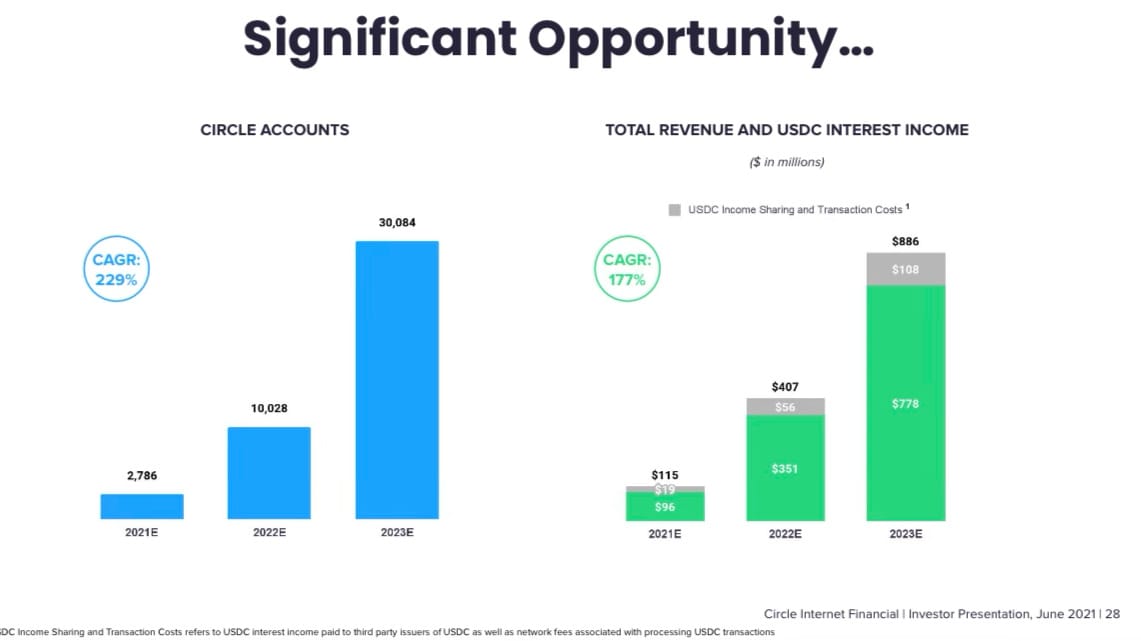

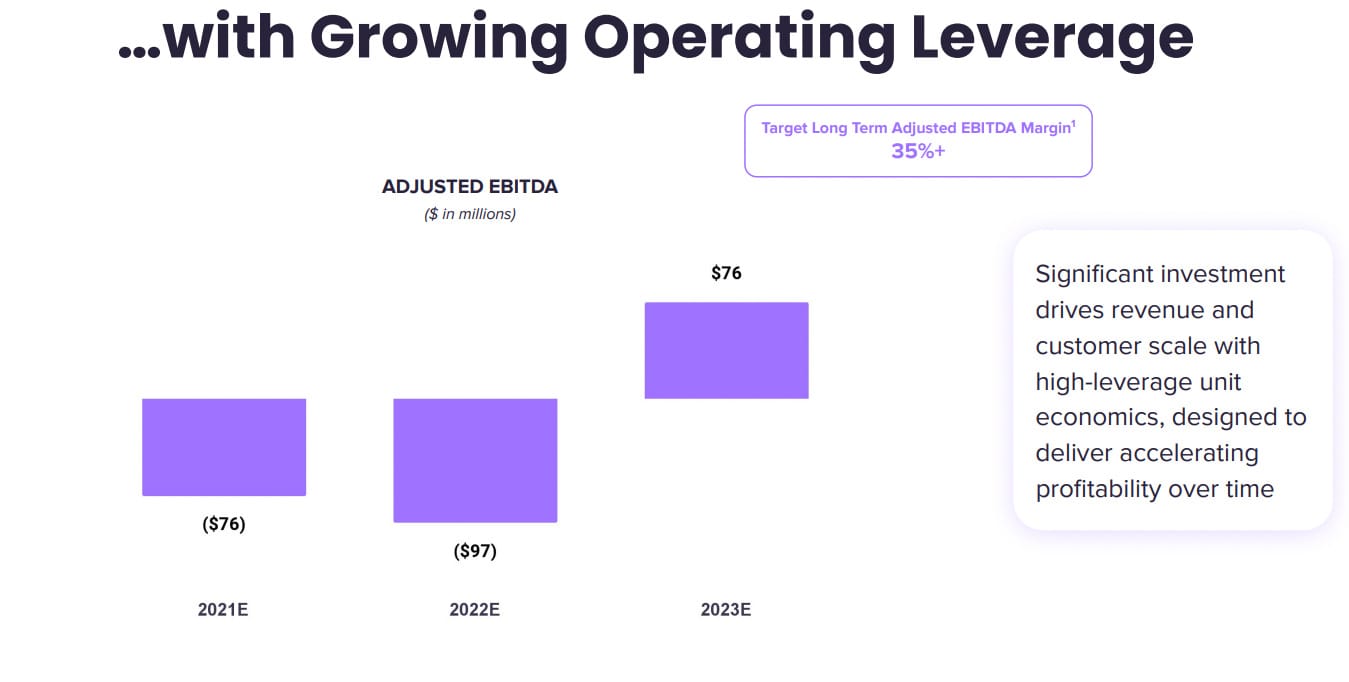

Back in 2018, Circle claimed they were profitable, but I can find no evidence nor statement to whether they still are. In fact, I have a great deal of evidence to suggest otherwise from pages 28 and 29 of their investor deck:

To explain the above - as of June 2021, during a bull market, Circle was predicted to lose $76 million. A year later, in 2022, and I am going to assume they thought the good times would never end, they projected that they would burn another $97 million. Magically, out of nowhere, justified by nothing, they would become profitable by tens of millions of dollars by end of 2023. And to be clear, these are “non-GAAP earnings,” meaning that these figures do not include non-recurring or non-cash expenses. And how will they do this? Why by simply tripling their account numbers! It’s just that easy!

Except it isn’t, because Circle was, and I would wager is burning cash. At the end of 2021, they had an operating loss of $86 million, with operating expenses of $128 million. A large chunk of their revenue came from interest yields on USDC - $28.4m - with $47.5m of income from transaction and treasury services around USDC itself. While I’m not going to dig too far into the rest of their form S-4 filed in May 2022, nothing about anything in there suggests that this is a company that will make more money than they spend anytime soon.

The Nightmare Scenario

My general sense here is that something is very much up with Circle and Coinbase, the two members of the consortium that invested in and runs USDC. From the S-4:

As part of our and Coinbase’s investment in the development of the Centre Consortium, we entered into agreements with Coinbase, pursuant to which we share any revenue generated from USDC reserves pro rata based on (i) the amount of USDC distributed by each respective party and (ii) the amount of USDC held on each respective party’s platform (i.e. held in its customers’ accounts) in relation to the total amount of USDC in circulation (the “Revenue Share Arrangement”).

Let’s cut to the chase: running USDC is not profitable. Circle is not profitable. Coinbase is not profitable, and had an operating loss of $554 million in Q1 2022. Despite the billions of dollars of issued USDC, the actual fundamental fabric of USDC is directly reliant on two unprofitable enterprises that partially make their money from the success of USDC as a stablecoin, which is largely predicated on institutional and retail investors wanting to buy, hold or transact with it, and then not cashing it out.

I can find very little about the Centre Consortium that controls USDC, but it seems that Circle has all but assumed responsibility for handling it based on the $400 million they raised from Blackrock earlier this year. I can’t find out what it costs to maintain, who is actually charged with maintaining it, and what the repercussions are for those who fail to do so. USDC is a fake currency issued by a consortium of two unprofitable for-profit companies, and while it’s good that it’s collateralized - the bare minimum one should expect from something that is meant to equal one dollar - its “principal operator” Circle is incredibly brittle, burning money every year with no end in sight.

From what I can tell, Circle’s operating costs for running USDC could be either $11.89m (“USDC income sharing and transaction costs”) or $30.73m (“Transaction and Treasury services costs”). Unless I am horribly wrong and the actual costs are somewhere else, these numbers range from “bad” to “awful,” making up a significant amount of Circle’s already-in-the-red costs. And these numbers are from 2021 - when things were actually good for crypto.

According to the USDC developer page, your funds are safe if Circle goes bankrupt:

However, one might reasonably postulate that if Circle does go bankrupt, the logical response is to assume that even if funds are “safe,” they may not be accessible. Voyager has $350 million in custodial funds that they have yet to return to customers, and that’s a drop in the bucket compared to the fifty billion dollars of USDC. In the (hopefully unlikely) event of a Circle bankruptcy or collapse, investors would likely want to get their money now, and even be willing to take a haircut to escape what they see as a weeks or months-long wait for liquidity.

While it may reassure you that Circle has actually got the dollars in the bank to support a potential bank run on USDC, what should bother you is the endless burn of cash. Circle is not a sustainable business, and failed to turn a profit even during the single easiest time to do so in cryptocurrency history. Circle is the company that promotes, maintains and builds USDC, meaning that if something happens to Circle, one could reasonably decide that one USDC does not equal a dollar, whether or not there are dollars in the bank to trade it for.

In June, Circle CEO Jeremy Allaire spoke to the Associated Press, and said that “market turmoil has been a really positive catalyst for USDC. It has been the flight to safety for crypto.” The problem is that while this safety may exist in USDC, USDC’s safety only goes as far as Circle can remain standing, and they have proven time and time again that running USDC itself is not profitable and is by proxy unsustainable.

Perhaps I’m wrong. Maybe Circle is capable of lumbering on, raising hundreds of millions of dollars of capital to keep their unprofitable, lumbering entity going until somebody works out a way to make more money. Maybe Coinbase is able to turn a profit again, and put that money into propping up USDC’s infrastructure. Maybe, even if Circle did fall apart, there would be somebody to scoop up these assets and keep running USDC - but that would require a gargantuan effort and absolutely tank the value of the token. Even if $40 million or so of operating costs a year isn’t much, the process of changing the guardian of USDC would crush any remaining trust.

However, I wouldn’t be surprised if their strategy was to simply be too big to fail - that, like Tether, nobody would actually let Circle die, because doing so would be so damaging for the cryptocurrency markets.