Yesterday, the Wall Street Journal ran a story about how Anthropic is “about to have its first profitable quarter,” specifically an operating profit, or EBITDA profitability:

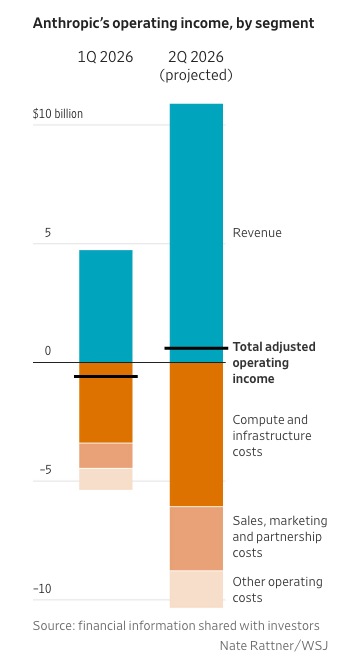

Anthropic’s revenue is set to more than double to $10.9 billion in the second quarter, an explosive rate of growth that will help it turn an operating profit for the first time.

…

Anthropic generated $4.8 billion in sales in the first quarter. Its quarterly revenue is now growing faster than Zoom did during the pandemic, and Google and Facebook in the run-up to their initial public offerings. It is set to turn an operating profit of $559 million in the June quarter.

Interesting! That’s a lot of certainty considering we’re barely through the first half of the second quarter, and quite a specific number given the fact that June hasn’t started! And all of these numbers are mysteriously leaking exactly while it raises its funding round!

Oh there’s also one important note: The Journal adds at the bottom of the article that “...it is unclear what accounting methods Anthropic has used to book revenue and costs, as the company isn’t yet required to follow the financial-reporting requirements of a public company.” That’s right —-- Anthropic is possibly going to be EBITDA profitable for a single quarter, on a non-GAAP basis.

Anyway, I wonder how Anthropic did it? Because based on this unhelpfully-labeled diagram from the Journal, it appears (as I said last year) that its costs scale linearly with its revenues, except they…magically didn’t in the second quarter?

I wonder if it'll stay profitable?

The company might not remain profitable for the full year as it plans spending increases due to its vast computing needs.

That’s also interesting. So Anthropic may be profitable very specifically in Q2 2026, but might not be afterward. It’s almost as if it found a way to specifically cut its costs in May and June somehow…

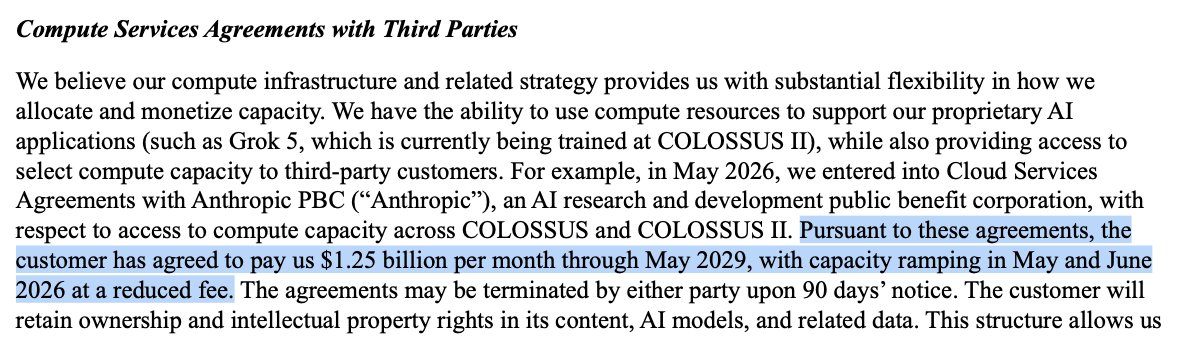

…because it did! Remember that deal Anthropic signed with SpaceX to take over Colossus-1? Well it’s also taking over some or all of Colossus-2, paying SpaceX $1.25 billion a month starting in May and June… when it’ll have a reduced fee as it ramps up!

That’s $15 billion a year in compute costs, but reduced to an indeterminately-discounted level for the precise months that Anthropic is using to tell investors and the media that it has an operating profit. That operating profit is a result of accountancy rather than any improvements to its business model.

While I wouldn’t say this is cooking the books, it’s definitely a shiatsu-grade massaging of the numbers. Anthropic has deliberately leaked a quarterly “profit” where it knows it can suppress its costs, specifically made sure that the journalist gave it the out of “costs might increase,” and released it on the day of NVIDIA’s earnings as a means of keeping the AI bubble inflated.

Nothing has changed.

If Anthropic paid full-rate for its compute in those two months, its economics would shift back to what they’ve always been per my reporting from last year on its AWS costs — a business that has costs that linearly increase with its revenue growth.

I also severely doubt that Anthropic managed to make the cost of running its services profitable in the space of six months.

Per The Information in January, Anthropic missed on its gross margin projections, saying that its inference costs were 23% higher than the company had anticipated.

How did Anthropic, which faced a massive influx of new business to the point that Anthropic was forced to buy more compute from Elon Musk, magically become profitable? Other than that discount, of course.

I have a few guesses:

- For large enterprises, Anthropic is taking prepayment of tokens —-- say, $50 million intended to be spread over 12 months that it takes in as revenue.

- This would both inflate revenue numbers and depress costs, because Anthropic wouldn’t have actually provided the compute necessary to earn that revenue yet.

- Anthropic is already offering discounted tokens for Claude users through the “buy extra credits” page on their accounts, with discounts ranging from 10% to 30%. It may very well be booking this up-front.

- Anthropic could be front-loading annual commitments of any kind —– subscriptions to Claude, enterprise or team agreements, and so on.

- Anthropic could have ratcheted down training to ease the burden on its infrastructure to provide inference.

Nevertheless, the revenue side is where the real problems lie.

The Numbers Don’t Add Up

So, Anthropic has said it brought in $4.8 billion in revenue in Q1 2026, and projects to hit $10.9 billion in Q2 2026.

This is tough to reconcile with previous reporting.

On February 12, 2026, Anthropic claimed it had reached $14bn in annual recurring revenue (ARR). As a reminder, ARR is an accounting tool largely used primarily by startups, where a snapshot of a single month’s income is taken and multiplied by twelve. This gives you an implied monthly revenue of roughly $1.17bn.

On March 3, 2026, Dario Amodei would claim Anthropic had reached $19bn in ARR — which works out to $1.58bn per month. Two days later, on March 9, Krishna Rao — Chief Financial Officer at Anthropic — would declare under oath in a court filing that Anthropic had brought in revenues “exceeding $5 billion to date.”

Keep in mind that The Information had previously reported that Anthropic had $4.5 billion in revenue in 2025, which I already found difficult to match with Rao's statements.

While boosters may claim that “exceeding” could mean literally any number they want above $5 billion, I find it doubtful that the CFO of Anthropic would, under oath, lead the court to believe its business was 30% to 40% smaller than it was, especially when trying to convince it that the damage of being labeled a supply chain risk would ruin its business.

At this point it’s impossible to reconcile the 2025 reporting with that $5 billion number. If we assume that the ARR claims made by Anthropic are correct, we can presume that it made revenues of roughly $2.5bn in March (given that it claimed it had $30 billion in ARR on April 6), $1.58bn in February, and $1.17bn in January, for a total of $5.25 billion.

I realize that figure is in excess of what the Wall Street Journal had and, in some world, those numbers could be cherry-picked using particular periods to the point that the real revenues would be in the region of $4.8 billion. That's possible.

But they don’t make a lick of sense when you bring up what Krishna Rao said. If we believe Anthropic’s leaks —-- putting aside all of the ARR figures for a second —-- this means that Anthropic:

- Made over 90% of its lifetime revenues in the first quarter of 2026.,

- Made virtually no revenue in its previous years, and…

- Leaked completely imaginary run rates to the media for years.

While I acknowledge that Anthropic has grown significantly, that level of stratospheric growth does stretch the limits of credibility. Moreover, the fact that previous ARR figures are inconsistent with the leaked charts from Anthropic further raises questions about the credibility of any numbers from the company.

The only real defense that anybody has here is that Krishna Rao, under oath, lowballed the US government and a judge to such a dramatic extent that he hid in excess of $4 billion in revenue.

And as I’ve discussed before — and FlyingPenguin helpfully collated — adding up Anthropic’s previously-reported ARR from January 2025 to March 3, 3rd 2026 already gets us to around $6.66 billion.

What Do You Really Think Is Happening Here?

I can imagine this has felt like a big victory for boosters — proof that AI can be profitable, that inference is profitable, that some sort of business model is emerging…and I’m sorry, that’s not what’s happening.

Dario Amodei and Elon Musk worked out a sweetheart deal, which they - framed as a “ramp-up,” - that allowed Anthropic to artificially depress its costs. I also question how much of a ramp-up there really was, or what Anthropic’s actual compute constraints were, because it immediately loosened rate limits for Claude subscribers on announcing the deal, meaning that it immediately started having higher inference costs, which…somehow led to it making a higher profit? Or did Musk — as literally described in its S-1 — have SpaceX charge Anthropic less for two specific months to make the numbers look better?

In July, Anthropic will start paying SpaceX $1.25 billion a month, - or $15 billion a year, - on top of all of its other compute deals with Google, Amazon and Microsoft.

If we assume that its spend is comparable on AWS and Google Cloud — and it’s most-assuredly more! — that means Anthropic is spending around $3.75 billion in compute costs, or $11.25 billion a quarter, or $45 billion a year.

There’s also a very compelling argument that Anthropic’s costs will increase and will eat up that profitability, to once again quote the Wall Street Journal:

The company might not remain profitable for the full year as it plans spending increases due to its vast computing needs.

I also have to wonder: if you’re so profitable, why not IPO? Why not take this to the public markets?

Unless, of course, you’re only non-GAAP EBITDA profitable based on a two-month-long discount specifically covering the period in which you’re profitable. And, of course, when you’re not a publicly-traded company, and so you don’t actually have to publish any numbers (and no, leaking them doesn’t count), and you’re not subject to SEC oversight.

I will give Dario Amodei credit: nobody does financial engineering and a press-led information war better than Anthropic. The willingness of the press to eat up incongruent numbers and the eagerness of many to jump up and find obtuse ways to explain away the obvious problems is only made possible when a company has perfected the art of manipulation and ingratiation of those who want to feel like they’re “first.”

If you take this as incontrovertible proof that Anthropic is profitable, you are deliberately ignoring the blatantly obvious ways these numbers are being massaged. We’ve got its CFO saying numbers that don’t match up with these leaks or Anthropic’s own marketing materials, and the aggressive and deluded way in which many people ignore them is equal parts frustrating and depressing.

To The AI Boosters In The Audience

Let me speak directly and with more empathy than usual: if you want Anthropic to win, you should be just as skeptical of these numbers as I am. You should want to smash my face in the tarmac with the most crystal-clear, impossible-to-argue with numbers, bereft of asterisks or discounts from suppliers or obfuscated accounting metrics.

You should want better from your heroes. If you truly think this company is amazing, unstoppable, and leading the tech industry to a glorious era of innovation, there shouldn’t be this many questions, and the metrics shouldn’t be this murky.

Every other time when a company has played this level of silly, weird bullshit has led to disaster — for example, WeWork claimed to be profitable since the second month of its operations, and repeated claims of profitability throughout its existence, and it turned out that it was only “profitable” if you removed things like “some of the costs of doing business.”

I get why you’re so defensive, and I get why you want this to work. A lot of you are very excited about generative AI, and being excited about it has given you a tremendous community of equally-excited people. I get that you like these tools.

And I need you to know these companies are laughing at you.

Anthropic timed this leak to focus on a specific quarter where it artificially suppressed costs, and gave you the flimsiest proof imaginable, specifically-crafted for you to share it as a triumph and spread the idea that “AI labs are actually profitable,” when their core economics haven’t changed. Costs increase linearly with revenue, and will continue to do so in perpetuity.

I genuinely can’t wait for both OpenAI and Anthropic to file their S-1s.

If you liked this piece, you should subscribe to my premium newsletter. It’s $70 a year, or $7 a month, and in return you get a weekly newsletter that’s usually anywhere from 5,000 to 18,000 words, including vast, detailed analyses of NVIDIA, Anthropic and OpenAI’s finances, and the AI bubble writ large. My Hater's Guides To Private Credit and Private Equity are essential to understanding our current financial system, and my guide to how OpenAI Kills Oracle pairs nicely with my Hater's Guide To Oracle.

This week, I’ll publish the second part to my ongoing series (“What If…We’re In An AI Bubble?”) about the factors and events that will cause the AI bubble to finally pop.

Subscribing to premium is both great value and makes it possible to write large, deeply-researched free pieces every week.