Soundtrack: The Dillinger Escape Plan — Black Bubblegum

To understand the AI bubble, you need to understand the context in which it sits, and that larger context is the end of the hyper-growth era in software that I call the Rot-Com Bubble.

Generative AI, at first, appeared to be the panacea — a way to create new products for software companies to sell (by connecting their software to model APIs), a way to sell the infrastructure to run it, and a way to create a new crop of startups that could be bought or sold or taken public.

Venture capital hit a wall in 2018 — vintages after that year are, for the most part, are stuck at a TVPI (total value paid in, basically the money you make for each dollar you invested) of 0.8x to 1.2x, meaning that you’re making somewhere between 80 cents to $1.20 for every dollar.

Before 2018, Software As A Service (SaaS) companies had had an incredible run of growth, and it appeared basically any industry could have a massive hypergrowth SaaS company, at least in theory. As a result, venture capital and private equity has spent years piling into SaaS companies, because they all had very straightforward growth stories and replicable, reliable, and recurring revenue streams.

Between 2018 and 2022, 30% to 40% of private equity deals (as I’ll talk about later) were in software companies, with firms taking on debt to buy them and then lending them money in the hopes that they’d all become the next Salesforce, even if none of them will. Even VC remains SaaS-obsessed — for example, about 33% of venture funding went into SaaS in Q3 2025, per Carta.

The Zero Interest Rate Policy (ZIRP) era drove private equity into fits of SaaS madness, with SaaS PE acquisitions hitting $250bn in 2021. Too much easy access to debt and too many Business Idiots believing that every single software company would grow in perpetuity led to the accumulation of some of the most-overvalued software companies in history.

As the years have gone by, things slowed down, and now private equity is stuck with tens of billions of dollars of zombie SaaS companies that it can’t take public or sell to anybody else, their values decaying far below what they had paid, which is a very big problem when most of these deals were paid in debt.

To make matters worse, 9fin estimates that IT and communications sector companies (mostly software) accounted for 20% to 25% of private credit deals tracked, with 20% of loans issued by public BDCs (like Blue Owl) going to software firms.

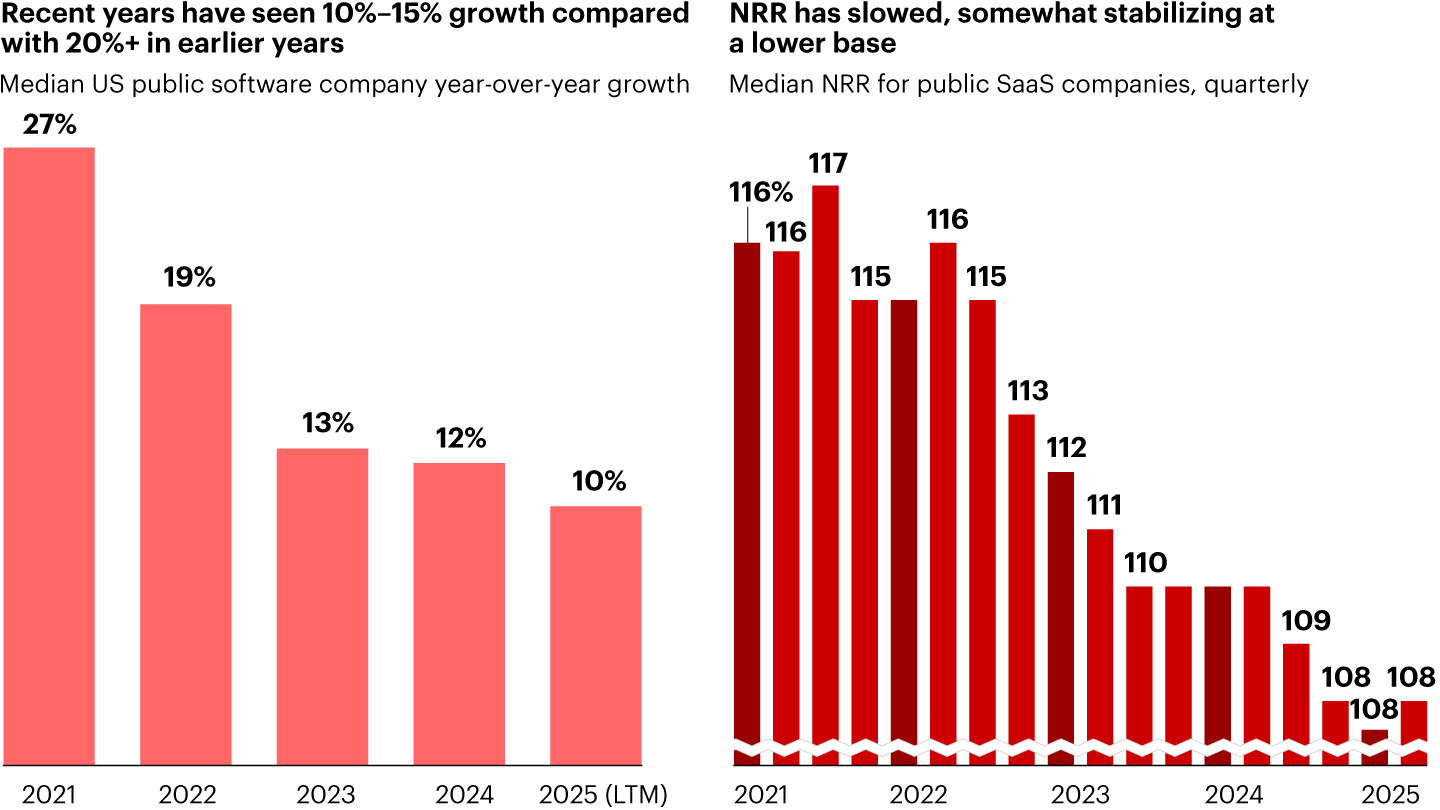

Things look grim. Per Bain, the software industry’s growth has been on the decline for years, with declining growth and Net Revenue Retention, which is how much you're making from customers and expanding their spend minus what you're losing from customers leaving (or cutting spend):

It’s easy to try and blame any of this on AI, because doing so is a far more comfortable story. If you can say “AI is causing the SaaSpocalypse,” you can keep pretending that the software industry’s growth isn’t slowing.

That isn’t what’s happening.

No, AI is not replacing all software. That is not what is happening. Anybody telling you this is either ignorant or actively incentivized to lie to you.

The lie starts simple: that the barrier to developing software is “lower” now, either “because anybody can write code” or “anybody can write code faster.” As I covered a few weeks ago…

Building software is not writing code and then hitting enter and a website appears, requiring all manner of infrastructural things (such as "how does a customer access it in a consistent and reliable way," "how do I make sure that this can handle a lot of people at once," and "is it quick to access," with the more-complex database systems requiring entirely separate subscriptions just to keep them connecting).

Software is a tremendous pain in the ass. You write code, then you have to make sure the code actually runs, and that code needs to run in some cases on specific hardware, and that hardware needs to be set up right, and some things are written in different languages, and those languages sometimes use more memory or less memory and if you give them the wrong amounts or forget to close the door in your code on something everything breaks, sometimes costing you money or introducing security vulnerabilities.

…

And yet, the myth that LLMs are an existential threat to existing software companies has taken root in the market, sending the share prices of the legacy incumbents tumbling.

From what I can gather, the other idea is that AI can “simply automate” the functions of a traditional software company, and “agents” can replace the entire user experience, with users simply saying “go and do this” and something would happen. Neither of these things are true, of course — nobody bothers to check, and nobody writing about this stuff gives a fuck enough to talk to anybody other than venture capitalists or CEOs of software companies that are desperate to appeal to investors.

To be more specific, the CEOs that you hear desperately saying that they’re “modernizing their software stack for AI” are doing so because investors, who also do not know what they are talking about, are freaking out that they’ll get “left behind” because, as I’ve discussed many times, we’re ruled by Business Idiots that don’t use software or do any real work.

There are also no real signs that this is actually happening. While I’ll get to the decline of the SaaS industry’s growth cycle, if software were actually replacing anything we’d see direct proof — massive contracts being canceled, giant declines in revenue, and in the case of any public SaaS company, 8K filings that would say that major customers had shifted away business from traditional software.

Midwits with rebar chunks in their gray matter might say that “it’s too early to tell and that the contract cycle has yet to shift,” but, again, we’d already have signs, and you’d know this if you knew anything about software. Go back to drinking Sherwin Williams and leave the analysis to the people who actually know stuff!

We do have one sign though: nobody appears to be able to make much money selling AI, other than Anthropic (which made $5 billion in its entire existence through March 2026 on $60 billion of funding) and OpenAI (who I believe made far less than $13 billion based on my own reporting.)

In fact, it’s time to round up the latest and greatest in AI revenues. Hold onto your hats folks!

Everybody’s AI Revenues Are Either Non-Existent Or A Secret

- In its Q4 2025 earnings, IBM said its total “generative AI book of business since 2023” hit $12.5 billion — of which 80% came from its consultancy services, which consists mostly of selling AI other people’s AI models to other businesses. It then promptly said it would no longer report this as a separate metric going forward.

- To be clear, this company made $67.5 billion in 2025, $62.8 billion in 2024, $61.9 billion in 2023 and $60.5 billion in 2022. Based on those numbers, it’s hard to argue that AI is having much of an impact at all, and if it were, it would remain broken out.

- Scummy consumer-abuser Adobe tries to scam investors and the media alike by referring to “AI-influenced” revenue — referring to literally any product with a kind of AI-plugin you can pay for (or have to pay for as part of a subscription) — and “AI-first” revenue, which refers to actual AI products like Adobe Firefly.

- It’s unclear how much these things actually make. According to Adobe’s Q3 FY2025 earnings, “AI-influenced” ARR was “surpassing” $5 billion (so $1.248 billion in a quarter, though Adobe does not actually break this out in its earnings report), and “AI-first” ARR was “already exceeding [its] $250 million year-end target,” which is a really nice way of saying “we maybe made about $60 million a quarter for a product that we won’t shut the fuck up about.”

- For some context, Adobe made $5.99 billion in that quarter, which makes this (assuming AI-first revenue was consistent) roughly 1% of its revenue.

- Adobe then didn’t report its AI-first revenue again until Q1 FY2026, when it revealed it had “more than tripled year over year” without disclosing the actual amount, likely because a year ago its AI-first revenue was $125 million ARR, but this number also included “add-on innovations.” In any case, $375 million ARR works out to $31.25 million a month, or (even though it wasn’t necessarily this high for the entire quarter) $93.75 million a quarter, or roughly 1.465% of its $6.40 billion in quarterly revenue in Q1 FY2026.

- Bulbous Software-As-An-Encumberance Juggernaut Salesforce revealed in its latest earnings that its Agentforce and Data 360 (which is not an AI product, just the data resources required to use its services) platforms “exceeded” $2.9 billion…but that $1.1 billion of that ARR came from its acquisition of Informatica Cloud, (which is not a fucking AI product by the way!). Agentforce ARR ended up being a measly $800 million, or $66 million a month for a company that makes $11.2 billion a year. It isn’t clear whether what period of time this ARR refers to.

- Microsoft, Google and Amazon do not break out their AI revenues.

- Box — whose CEO Aaron Levie appears to spend most of his life tweeting vague things about AI agents — does not break out AI revenue.

- Shopify, the company that mandates you prove that AI can’t do a job before asking for resources, does not break out AI revenue.

- ServiceNow, whose CEO said back in 2022 told his executives that “everything they do [was now] AI, AI, AI, AI, AI,” said in its Q4 2025 earnings that its AI-powered “Now Assist” had doubled its net new Annual Contract Value had doubled year-over-year,” but declined to say how much that was after saying in mid-2025 it wanted a billion dollars in revenue from AI in 2026.

- Apparently it told analysts that it had hit $600 million in ACV in March (per The Information)...in the fourth quarter of 2025, which suggests that this is not actually $600 million of revenues quite yet, nor do we know what that revenue costs.

- What we do know is that ServiceNow had $3.46 billion in 2025, and its net income has been effectively flat for multiple quarters, and basically identical since 2023.

- Intuit, a company that vibrates with evil, had the temerity to show pride that it had generated "almost $90 million in AI efficiencies in the first half of 2025,” a weird thing to say considering this was a statement from March 2026. Anyway, back in November 2025 it agreed to pay over $100 million for model access to integrate ChatGPT. Great stuff everyone.

- Workday, a company that makes about $2.5 billion a quarter in revenue, said it “generated over $100 million in new ACV from emerging AI products, [and that] overall ARR from these solutions was over $400 million.” $400 million ARR is $33 million.

- Atlassian, which just laid off 10% of its workforce to “self-fund further investment in AI,” does not break out its AI revenues.

Riddle me this, Batman: if AI was so disruptive to all of these software companies, would it not be helping them disrupt themselves? If it were possible to simply magic up your own software replacement with a few prompts to Claude, why aren’t we seeing any of these companies do so? In fact, why do none of them seem to be able to do very much with generative AI at all?

Sidenote: Also…where are the competitors? Where are the stories of companies building their own SaaS replacements? Software CEOs never, ever stop talking. Wouldn’t this be all they’d talk about? Klarna claimed it replaced its Salesforce contract with AI, and then had to hastily explain that the reason was that the company created its own internal CRM using graph database Neo4j, but of course couldn’t possibly share what it looked like. Lovable claims one of its customers replaced Salesforce with its CRM, running it entirely on Lovable’s services at a cost of $1200 a year, claiming “no ongoing maintenance complexity.” Reassuringly, the company’s CEO said that his “head of finance is more or less running it in his spare time.”

Curiously, said CRM looks very, very similar to open source CRM Twenty.

The point I’m making is fairly simple: the whole “AI SaaSpocalypse” story is a cover-up for a much, much larger problem. Reporters and investors who do not seem to be able to read or use software are conflating the slowing growth of SaaS companies with the growth of AI tools, when what they’re actually seeing is the collapse of the tech industry’s favourite business model, one that’s become the favourite chew-toy of the Venture Capital, Private Equity and Private Credit Industries.

You see, there are tens of thousands of SaaS companies in everything from car washes to vets to law firms to gyms to gardening companies to architectural firms. Per my Hater’s Guide To Private Equity:

For the best part of 20 years, software startups have been seen as eternal growth-engines. All you had to do was find a product-market fit, get a few hundred customers locked in, up-sell them on new features and grow in perpetuity as you conquered a market. The idea was that you could just keep pumping them with cash, hire as many pre-sales (technical person who makes the sale), sales and customer experience (read: helpful person who also loves to tell you more stuff) people as you need to both retain customers and sell them as much stuff as you need.

You’d eventually either take that company public or, in reality, sell it to a private equity firm. Per Jason Lemkin of SaaStr:

For years, PE was the reliable exit. Hit $20M in ARR, get to 40% growth or Rule of 40, and you’d see term sheets. From 2012 through 2023, nearly every company in the SaaStr Fund portfolio that crossed $20M ARR with solid fundamentals received multiple PE offers. It was the gift of exits that kept on giving. The multiples weren’t always great, but the offers came. Again and again and again.

That’s not happening anymore.

The problem is that SaaS valuations were always made with the implicit belief that growth was eternal, just like the rest of the Rot Economy, except SaaS, at least for a while, had mechanisms to juice revenues, and easy access to debt. After all, annual recurring revenues are stable and reliable, and these companies were never gonna stop growing, leading to the creation of recurring revenue lending:

Financing for private equity buyouts of these businesses comes mostly from private credit investors. It’s usually via annual recurring-revenue (ARR) loans, with loan amounts set at a multiple of annualized recurring revenue. For example, a software company with recurring revenues of $100 million seeking a loan of twice that amount would borrow $200 million.

To be clear, this isn’t just for leveraged buyout situations, but I’ll get into that later. The point I’m making is that the setup is simple:

- Tens of thousands of SaaS companies were created in the last 20 years.

- These companies, for a while, had what seemed to be near-perpetual growth.

- This led to many, many private equity buyouts of SaaS companies, pumping them full of debt based on their existing recurring revenue and the assumption that they would never, ever stop growing.

- I will get into this later. It’s very bad.

- When growth slowed, the reaction was for these companies to raise venture debt — loans based on their revenue — and per Founderpath, 14 of the largest Business Development companies loaned $18 billion across 1000 companies in 2024 alone, with an average loan size of $13 million.

- This includes name brand companies like Cornerstone OnDemand and Dropbox, the latter of which took on a $34.4 million debt facility with an 11% interest rate. One has to wonder why a company that had $643 million in revenue in Q4 2024 needed that debt.

You see, nobody wants to talk about the actual SaaSpocalypse — the one that’s caused by the misplaced belief that any software company will grow forever.

Generative AI isn’t destroying SaaS. Hubris is.

A Brief Guide To SaaS

Alright, let’s do this one more time.

SaaS — Software As A Service — is both the driving force and seedy underbelly of the tech industry. It’s a business model that sells itself on a seemingly good deal. Instead of paying upfront for an expensive software license and then again when future updates happen, you pay a “low” monthly fee that allows you to get (in theory) the most up-to-date (in theory) and well-maintained (in theory) version of whatever it is you’re using. It also (in theory) means that companies need to stay competitive to keep your business, because you’re committing a much smaller amount of money than a company might make from a single license.

Over here in the real world, we know the opposite is true. Per The Other Bubble, a piece I wrote in September 2024:

Core to the business models of multiple tech companies is the humble "SaaS" (software as a service) model, where you're charged a monthly amount on a per-user basis for some sort of cloud-based software that you neither own nor control. To be clear, there's nothing inherently wrong with SaaS. For businesses, it reduces costs by removing the need to run their own infrastructure and employ people to maintain it. It can run theoretically from anywhere and costs are measurable, predictable, and adaptable to the organization's size. And, crucially, businesses don’t have to pay upfront for a license — which can cost thousands, or tens of thousands — and spread the cost across the life of the application.

You can see the appeal. SaaS is one of the most dominant business models in tech, because it fits both the customer profile of "not wanting to run a bunch of infrastructure" and the tech industry's love of trapping people in distinct ecosystems that are hard to escape. While SaaS is generally a good deal for small-to-mid-sized companies, the inevitable sprawl of letting SaaS into your organization means that you're stuck with them.

While managing 100 accounts might be something that your organization can do alone, how are you going to manage 1000? Or 10,000? Managing SaaS applications is a time-consuming and tedious process for large businesses, and now there are even — you guessed it — SaaS applications that can do it for you. What happens if your organization is in Europe and needs to be GDPR-compliant? What happens if you need to make sure your data is held on a server entirely separate to the rest of the company's business? While some SaaS companies offer private cloud (where the application exists on its own dedicated AWS or Azure instance), giving companies the flexibility to choose where and how to store their data, many don’t.

This is the devil's deal of the Software-As-A-Service market (and SaaS spend is expected to crest over $230 billion in 2024). While the convenience of not having to build your own distinct software run on its own distinct hardware is great, or having to pay ungodly sums upfront for software licenses, you are also effectively outsourcing your entire organization's functionality to another company. With every new integration, every new seat, every new add-on their sales team makes you pay for and every new product they graciously train your staff to use, your organization becomes more burdened by the beast of SaaS.

The bigger you are — or the longer you stay — the more powerful the parasite becomes, eventually burdening your organization to the point that you are effectively only as innovative as the SaaS provider you're anchored to.

It’s hard to say exactly how large SaaS has become, because SaaS is in basically everything, from whatever repugnant productivity software your boss has insisted you need, to every consumer app now having some sort of “Plus” package that paywalls features that used to be free. Nevertheless, “SaaS” in most cases refers to business software, with the occasional conflation with the nebulous form of “the enterprise,” which really means “any company larger than 500 people.”

McKinsey says it was worth “$3 trillion” in 2022 “after a decade of rapid growth,” Jason Lemkin and IT planning software company Vena say it has revenues somewhere between $300 billion and $400 billion a year. Grand View Research has the global business software and services market at around $584 billion, and the reason I bring that up is that basically all business software is now SaaS, and these companies make an absolute shit ton on charging service fees. “Perpetual licenses” — as in something you pay for once, and use forever — are effectively dead, with a few exceptions such as Microsoft Windows, Microsoft Office, and some of its server and database systems. Adobe killed them in 2014 (and a few more in 2022), Oracle killed them in 2020, and Broadcom killed them in 2023, the same year that Citrix stopped supporting those unfortunate to have bought them before they went the way of the dodo in 2019.

To quote myself again, in 2011, Marc Andreessen said that “software is eating the world.” And he was right, but not in a good way. Andreesen’s argument was that software should eat every business model:

…have you ever used a piece of software at a company you work for that sucks? Was it sold by Microsoft, Salesforce, Google, Atlassian or another big SaaS company? Well, it was probably bought by somebody who doesn't use the software, and it'll cost far more to remove than your annoyance matters. The burdensome presence of software like Microsoft Teams or Salesforce Platform in your life is a result of these organizations using brand recognition to sell into your organization, and once they're in there, their sales teams exist to continually find ways to increase the revenue of each user. The people making the decisions about the software you use — usually C-level executives — are doing so based on a sales pitch tailored to them and their preconceptions of what your job is rather than any firm experience, and thus they will sign year(s) long contracts based on a great sales pitch and the financials that "make sense."

Every single company you work with that has any kind of software now demands you subscribe to it, and the ramifications of them doing so are more significant than you’ve ever considered.

That’s because SaaS is — or, at least, was — a far-more-stable business model than selling people something once. Customers are so annoying. When they buy something, they tend to use it until it stops working, and if you made the product well, that might mean they only pay you once.

SaaS fixes this problem by giving them only one option — to pay you a nasty little toll every single month, or ideally once a year, on a contractual basis, in a way that’s difficult to cancel.

Sadly, the success of the business software industry turned everything into SaaS.

Recently, I tried to cancel my membership to Canva, a design platform that sort of works well when you want it to but sometimes makes your browser crash. Doing so required me to go through no less than four different screens, all of which required me to click “cancel” — offers to give me a discount, repeated requests to email support, then a final screen where the cancel button moved to a different place.

This is nakedly evil. If you are somebody high up at Canva, I cannot tell you to go fuck yourself hard enough! This is a scummy way to make business and I would rather carve a meme on my ass than pay you another dollar! It’s also, sadly, one of the tech industry’s most common (and evil!) tricks.

Everybody got into SaaS because, for a while, SaaS was synonymous with growth. Venture capitalists invested in business with software subscriptions because it was an easy way to say “we’re gonna grow so much,” with massive sales teams that existed to badger potential customers, or “customer success managers” that operate as internal sales teams to try and get you to start paying for extra features, some of which might also be useful rather than helping somebody hit their sales targets.

The other problem is how software is sold. As discussed in the excellent Brainwash An Executive Today, Nik Suresh broke down the truth behind a lot of SaaS sales — that the target customer is the purchaser at a company, who is often not the end user, meaning that software is often sold in a way that’s entirely divorced from its functionality. This means that growth, especially as things have gotten desperate, has come from a place of conning somebody with money out of it rather than studiously winning a customer’s heart.

And, as I’ve hinted at previously, the only thing that grows forever is cancer.

In today’s newsletter I am going to walk you through the contraction — and in many cases collapse — of tech’s favourite business model, caused not by any threat from Large Language Models but the brutality of reality, gravity and entropy. Despite the world being anything but predictable or reliable, the entire SaaS industry has been built on the idea that the good times would never, ever stop rolling.

I guess you’re probably wondering why that’s a problem! Well, it’s quite simple (emphasis mine):

The Apollo co-president pointed to the period from 2018 to 2022, when software accounted for 30% to 40% of the private market. During that era, investors assumed nearly 100% retention rates and minimal disruption risk, leading many small to medium-sized software businesses to be taken private based on assumptions that now appear questionable.

That’s right folks, 40% of PE deals between 2018 and 2022 were for software companies, the very same time venture capital fund returns got worse. Venture and private equity has piled into an industry it believed was taking off just as it started to slow down.

The AI bubble is just part of the wider collapse of the software industry’s growth cycle.

This is The Hater’s Guide To The SaaSpocalypse, or “Software As An Albatross.”